Explaining what Ripple is can be hard. To make things a little easier, we made a video!

For Ripple Labs, it’s an opportunity to share our vision of the Internet of money, show how Ripple fits into the equation, and highlight the tools and technology we’re building to make that vision a reality. It’s also a chance to show the world who we really are.

https://kinematec.de/wp-content/uploads/2015/01/anna-vahe.jpg435777christianhttps://kinematec.de/wp-content/uploads/2019/10/kinematec_logo.pngchristian2015-01-07 21:47:182015-01-12 07:24:39Building the Internet of Money (Video)

Throughout 2014 we’ve talked to businesses all over the world, both big and small, who are interested in tapping into Ripple’s increasing liquidity and settlement capabilities. For exchanges dealing in bitcoins and other assets, the value proposition is clear – deeper orderbooks and the ability for customers to hop between different assets instantly is a major boon to their service. The natural follow-up question is how to get started.

As such, we’ve developed a high-level integration guide for exchanges that covers the basic accounting concepts of operating a gateway on Ripple and some of the API calls you can use to interact with the network. For the purposes of this guide, we’ve outlined an example integration for the fictional Acme Bitcoin Exchange. While specifically referencing bitcoins as the asset handled by this gateway, note that the concepts are applicable to other forms of value such as physical commodities, securities, fiat currencies, and more.

Feel free to email us at with any questions or thoughts on how this could be improved.

https://kinematec.de/wp-content/uploads/2019/10/kinematec_logo.png00christianhttps://kinematec.de/wp-content/uploads/2019/10/kinematec_logo.pngchristian2015-01-07 12:53:212015-01-12 07:24:45Turn your exchange into a Ripple Gateway

For Ripple Labs, 2014 was the year in which we not only clarified our strategy for building the Internet of money but also made large strides in turning that vision into reality. From breakthrough partnerships to ecosystem expansion to the continued evolution of the underlying technology, 2014 has been a banner year. This is our year in review.

By the numbers

Major partnership announcements: 4 (3 banks, 1 network)

IRBA-certified Ripple gateways around the world: 16

24-hour network trade volume (all-time record): >$ 6.5 million

24-hour network trade volume (average, last 30 days): >$ 2 million

The New York Times, The Wall Street Journal, Bloomberg, Bloomberg Businessweek, CNBC, USA Today, Fox Business, The Financial Times, Fortune, Institutional Investor, Forbes, Business Insider, International Business Times, Entrepreneur, VentureBeat, American Banker, TechCrunch, GigaOm, PandoDaily

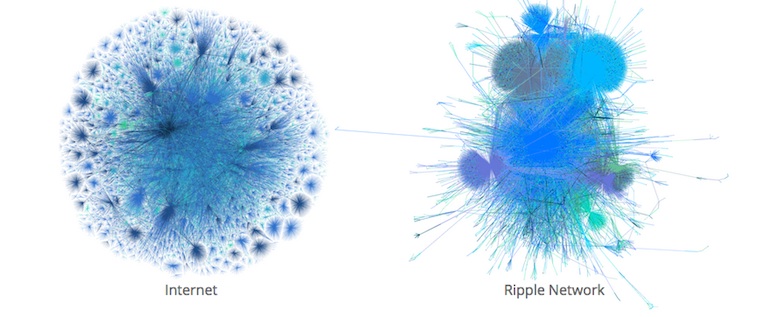

Navigating a startup working on brand new technology can be a perilous process. It can, at times, feel like you’re walking in the dark. But while it’s impossible to predict the future, we can look to the past for clues. In that regard, we see the state of payments tracking the history of the information web.

In September, Ripple Labs CTO Stefan Thomas published an op-ed in TechCrunch, outlining our vision for how the space will evolve, drawing parallels with the birth of the information web. Stefan breaks this evolution into three phases with each new phase building on the last.

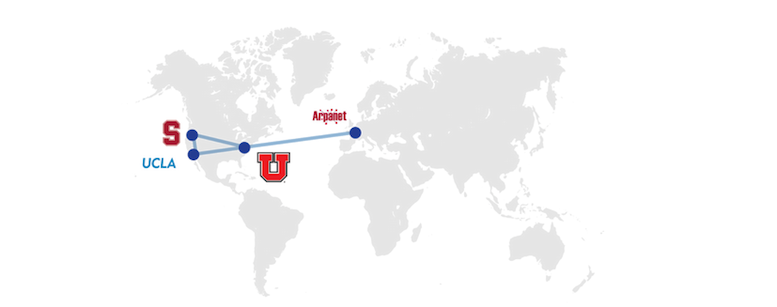

The Infrastructure Phase: The original custodians of information on the Internet were universities and research facilities like CERN. While the network was already open and global in scope, it was still limited from a consumer perspective. In the case of payments, custodians of money, such as banks and governments, will lay the initial groundwork and plumbing for value transfer.

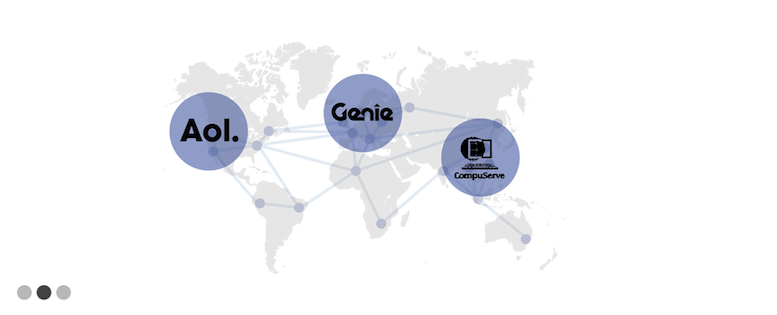

The Federation Phase: By the ‘80s, numerous services popped up to address increasing consumer demand, but these disparate networks originally weren’t interoperable. If you were on AOL, there wasn’t an easy way to connect with your friend on GEnie. This would be solved by the rise of common protocols like HTTP and SMTP that allowed networks to federate, bringing millions of consumers together all in one place. Similar to the Internet of the ‘80s, today’s payment networks aren’t yet federated, lacking a standardized protocol. Innovative services like Paypal, Alipay, and Venmo provide users with new features and convenience, but they also don’t interoperate. If you’re on Paypal, you can’t send your friend money if he or she is on Venmo.

The Independent Value Phase: With everyone on the same network, it wasn’t long before developers and entrepreneurs started building services and businesses like Wikipedia, Google, and Facebook. What’s most exciting is that it’s impossible to predict what inventive, pioneering new industries will blossom. We believe that the same will hold true for the Internet of money.

The year we refined market fit and gained traction

Now that we had a better sense of where we wanted to go, we needed to figure out how to get there. The strategy that we ultimately defined reflects our ongoing commitment at Ripple Labs to create tools and technology that empower financial institutions, businesses, and ultimately developers.

We’re starting where Ripple provides the biggest impact for payments companies, app developers and ultimately consumers—the core. Skipping this essential developmental chapter to deliver these tools and technologies directly to consumers would be putting the cart before the horse. Partnerships with financial institutions establish a platform and market that others can build on higher up the application stack by first producing general utility and stability.

Just as the Internet of information required necessary groundwork before the likes of Peter Thiel and Mark Zuckerberg could change the world with PayPal and Facebook, the Internet of money requires a preliminary framework.

On the one hand, we need the web browser, the smartphone, and ubiquitous Internet access. On the other hand—in the case of moving money—we need liquidity, compliance and scalability. In place of universities and government institutions, we have financial institutions, which custody assets and already move trillions of dollars daily to solidify the foundation of the value web. Because of Ripple’s open nature, builders will be able to leverage the power and potential of the existing system in unimaginable ways. Where today’s systems are closed, tomorrow’s will be more open.

This is an admittedly challenging, painstaking, and laborious process, but fortunately, Ripple Labs—with the help of its supporters, partners, and community—made great headway in 2014.

In May, we announced our partnership with Germany’s Fidor Bank, the first financial institution to integrate the Ripple protocol. Momentum kept building, leading up to Sibos, the annual financial services conference hosted by SWIFT.

To our pleasant surprise, Ripple was a persistent topic throughout the event, which attracted over 7,000 industry members. Where once potential partners worried about the reputational risk of integrating a brand new technology, now they were wondering how they could get started, perceiving innovation as a competitive advantage.

We got the sense that we were reaching a tipping point in terms of awareness within the financial community. This was particularly evident at a leadership workshop hosted by the World Economic Forum, which counted industry leaders like Deloitte, Barclays, and SWIFT. Again, many of the discussions centered around the Ripple protocol. During one presentation, a director of the Bill & Melinda Gates Foundation noted not only how Ripple could make cross-border payments more efficient but also how the technology could help address the ongoing issue of financial inclusion.

Fundamental to this strategy is the core technology that powers the Ripple protocol. In August, Ripple Labs released the consensus whitepaper, which describes the Ripple protocol’s consensus algorithm and properties.

Throughout 2014, the rippled team worked on improving stability, increasing rippled uptime to over 99 percent. The team also rolled out a series of new features and improvements including Account Freeze, transaction memos, and improvements to pathfinding. We’ve also completed development of features like Autobridging, which will be released in early 2015. Meanwhile, senior rippled developer Howard Hinnant completed his proposal relating to hashing infrastructure, which he submitted to the C++ Standards Body.

In all, the team made significant improvements to the stability, robustness, and value of the protocol.

The success we’ve experienced in 2014 in working with the existing industry was matched by grassroots efforts in our growing developer community. Today, developers and businesses have established Ripple gateways in every hemisphere. Along with the community, we also supported the establishment of the International Ripple Business Association, which provides best practice guidance to Ripple gateways and other businesses. The IRBA held its first officer elections this fall.

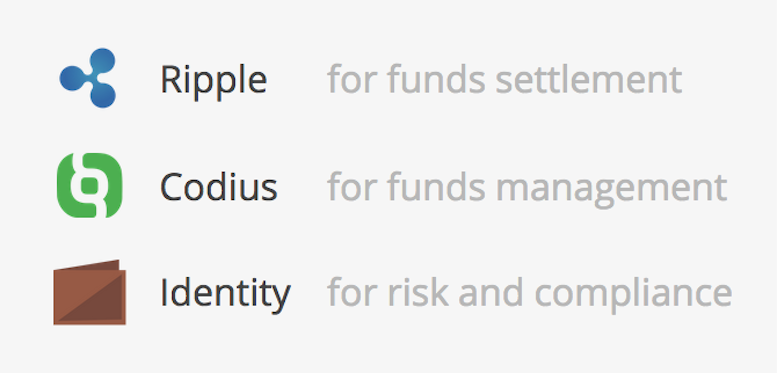

We realized early on this year that in order to achieve our mission of opening access to finance, we would need to build tools and platforms for business logic and identity management in addition to focusing on funds settlement.

Karen Gifford, chief compliance officer at Ripple Labs, summarized the opportunity for digital identity management in a Huffington Post op-ed. Today’s existing protocols for addressing the issue of identity simply come up short across the board. Not only is the way we deal with identity inefficient and costly, current procedures undermine both security and privacy by placing the onus on entities who aren’t security experts (like retailers and banks).

In collaboration with MIT and dozens of prominent industry members, Ripple Labs contributed to the creation of the Windhover Principles, a set of principles and a framework for approaching new solutions for addressing digital identity, trust, and access to shared, open data.

The other key puzzle piece is smart contracts, which enables the application of rule sets and automated execution of those rules to funds transfer. In July, Stefan Thomas and team unveiled Codius, an open-source, smart contracts platform. From a broader perspective, it’s a framework for developing distributed applications, what we call “smart programs.” Stefan and team member Evan Schwartz presented Codius during a Tech Talk at the Around the World in Five Seconds event last month.

While Ripple Labs has made great headway in 2014, the hard work has only just begun. We look forward to building on the team’s and community’s successes for years to come.

https://kinematec.de/wp-content/uploads/2015/01/yir-2014.jpg500777christianhttps://kinematec.de/wp-content/uploads/2019/10/kinematec_logo.pngchristian2015-01-06 20:29:432015-01-12 07:25:01Ripple Labs 2014: A Year in Review

Throughout 2014 we’ve talked to businesses all over the world, both big and small, who are interested in tapping into Ripple’s increasing liquidity and settlement capabilities. For exchanges dealing in bitcoins and other assets, the value proposition is clear – deeper orderbooks and the ability for customers to hop between different assets instantly is a major boon to their service. The natural follow-up question is how to get started.

As such, we’ve developed a high-level integration guide for exchanges that covers the basic accounting concepts of operating a gateway on Ripple and some of the API calls you can use to interact with the network. For the purposes of this guide, we’ve outlined an example integration for the fictional Acme Bitcoin Exchange. While specifically referencing bitcoins as the asset handled by this gateway, note that the concepts are applicable to other forms of value such as physical commodities, securities, fiat currencies, and more.

Feel free to email us at with any questions or thoughts on how this could be improved.

https://kinematec.de/wp-content/uploads/2019/10/kinematec_logo.png00christianhttps://kinematec.de/wp-content/uploads/2019/10/kinematec_logo.pngchristian2014-12-19 05:23:352015-01-12 08:33:27Turn your exchange into a Ripple Gateway

Explaining what Ripple is can be hard. To make things a little easier, we made a video!

For Ripple Labs, it’s an opportunity to share our vision of the Internet of money, show how Ripple fits into the equation, and highlight the tools and technology we’re building to make that vision a reality. It’s also a chance to show the world who we really are.

https://kinematec.de/wp-content/uploads/2014/12/anna-vahe.jpg435777christianhttps://kinematec.de/wp-content/uploads/2019/10/kinematec_logo.pngchristian2014-12-18 04:04:002015-01-12 07:31:44Building the Internet of Money (Video)

As interest in Ripple increases around the world, the ecosystem is steadily expanding into new and untapped markets. Recently, Minsung Park, a former lawyer and technology whiz brought Ripple to South Korea with the newest Ripple gateway, Pax Moneta.

Like many innovators building on the Ripple protocol, Mingsung’s history and breadth of experience is rich and unique, having helped to draft laws and write software that spurred the mass adoption of public key infrastructure within his home country.

“My parents wanted me to be a lawyer, so I became a lawyer,” said Minsung, who has helped translate various Ripple documents into Korean, such as the Ripple Primer (Korean). “But my basic instinct was toward science. It was my basic instinct that introduced me to the Internet. In my body and my soul, I am focused on this sort of scientific thinking.”

Minsung sees the potential of Ripple to help better connect his country and its citizens to the broader economic machine, reducing friction between neighboring markets, like China and Japan, as well as beyond, such as in the U.S. and Europe.

Tell us about yourself!

I was born in 1968 so I am 46. Sometimes I forget my age. I majored in law, with a focus on criminal law and information law. At the time, I remember the Internet was just introduced to Korea while I was in graduate school.

The concept quickly piqued my interest so I started digging. “What is the Internet?” I wanted to know. I discovered Mozilla. At the time, I was able to use a phone to connect to the Internet. One of the first things I did was create an Internet group at my university as part of the computer science and law departments, which ran a web server.

I completed my law major, but, personally, because of the Internet, I was interested in programming. From there, I ended up working at a government agency, the Korean Information Society Development Institute or KISDI. One of my primary responsibilities was to help formulate a law regarding the Korean Signature Act (1999) based on a public key system or PKI.

This was how I first came across the idea of a cryptocurrency, around 1996 or 1997, but I didn’t yet fully comprehend the meaning of currency or cryptocurrency. As time went on, I continued my research on the idea of the cryptographic key and kept on learning programming, including languages like C and C++. I ended up creating software for law firms working with government agencies, such as the Korea National Police Agency and the Korea Intelligence Services as well as other organizations using special cryptography with Western countries. Over time, many companies would integrate PKI, both for commercial and government websites in Korea.

I also ran a trading and development company with a focus in futures and options so I had an opportunity to live in the UK for around three years. Through that experience, I saw that the banking systems of Western countries were very developed and there was a good chance we could introduce these systems to Korea.

Three years ago, I returned to Korea, where I continued my study of cryptography, programming, and electronic trading. That’s when I read an article about Bitcoin, which brought back the idea of a cryptocurrency that I came across during my time with KISDI. I ran to the closest bookstore to learn more. During that search, I found Ripple, another way to transfer value digitally.

That’s when I started working on and developing a Ripple gateway, Pax Moneta, which is the first Ripple gateway in South Korea. Pax Moneta means “peace of money,” a clever play on words, originating from the term “Pax Romana” or “Pax America”

That’s quite a journey! What ended up attracting you to Ripple?

The reason why I created a Ripple company is simply because the technology is just great. It makes sense. In a way, Bitcoin is about replacing currency like the U.S. Dollar. On the other hand, Ripple is complementary and can help exchange any currency, KRW, CNY, GBP, or USD. That means Ripple can work with governments instead of against them. Personally, I will still use Bitcoin, but Ripple can be used as a method to help exchange value quickly between many countries.

So I have a lot of belief in Ripple, which I feel is supported by my background. I majored in law, but my basic instinct was always based on natural sciences. That’s why I love Ripple and I’m lucky because I think I can understand both areas.

What sort of challenges did you face?

I tried to build a rippled server. It was very difficult, but ultimately, I succeeded. Then I had to figure out how to use rippled, ripple-lib, and gatewayd.

One issue is that Node.js and Angular.js were very new to Koreans. Most developers in Korea are using Java. I couldn’t find a book in Korean for Angular.js so this was a challenge, but I was able to find English resources on the Internet. It was often difficult to sleep. If I’m interested in something, I cannot see anything, but this single passion.

After a bit of studying, I was able to better understand gatewayd and ripple-lib. A few months ago, my gateway was nearly ready so I contacted the International Ripple Business Association or IRBA.

Congratulations, that’s a huge accomplishment! Is the Ripple technology being embraced locally?

There have been some difficulties, primarily because most Koreans don’t know the existence of Ripple. We now have a gateway, but many Koreans don’t understand what a gateway is. So one thing we have to do is create a more intuitive Ripple client on top of gatewayd for Koreans to use.

Tell us about your team!

At the moment, we have four people, to cover programming, design, and marketing, but we are actively recruiting. We’re still small. We’re a startup.

Since one of the main challenges for Pax Moneta is Ripple mindshare in Korea, do you have an explicit marketing strategy?

As you know, Korea is located between China and Japan. Traditionally, KRW and USD has been essential to the Korean economy. I want to help Korea become a bridge between the USA and China. So in the long view, Pax Moneta should focus on these two countries.

There are many Koreans who own factories in China and there are also many Chinese people who want to come to Korea so there is high demand for exchange between KRW and CNY.

What’s the regulatory climate surrounding these technologies like in Korea?

There was a recent government petition on virtual currencies. In general, the view seems to be that virtual currencies are convenient, like Ripple, which is fast and operates within the law, but the price is not stable. So at the moment, the Bank of Korea does not have any explicit plan to support it.

As you may know, in Korea, the government plays a significant role in supporting companies so the issues of regulation are very important. But I believe it will be similar to adoption of the Internet. Today, the Internet is used by the Korean government. In the future, I think Ripple will be used, too. When my son and my grand children become parents, they will use virtual currencies.

The Korean government does block certain things, but in general, they want to support innovation, like with AG pay and Kakao pay. We’re entering a new era and I think there will be many chances in front of us if we are prepared for the future.

Any final thoughts?

Yes, just this: “If all roads lead to Rome, then all values lead to Ripple.”

https://kinematec.de/wp-content/uploads/2014/12/paxmoneta_logo_Blog2.png586777christianhttps://kinematec.de/wp-content/uploads/2019/10/kinematec_logo.pngchristian2014-12-08 23:20:322015-01-12 07:32:54Pax Moneta: South Korea’s First Ripple Gateway

The Stellar Development Foundation (SDF) which maintains Stellar, a network built on a modified version of the Ripple code base, recently published a post claiming flaws in the Ripple consensus algorithm. We take any reports about possible security issues very seriously and after reviewing the information conclude that there is no threat to the continued operation of the Ripple network. We’d like to share our thoughts.

Quoting the post in question:

Issue 1: Sacrificing safety over liveness and fault tolerance—potential for double spends

The Fischer Lynch Paterson impossibility result (FLP) states that a deterministic asynchronous consensus system can have at most two of the following three properties: safety (results are valid and identical at all nodes), guaranteed termination or liveness (nodes that don’t fail always produce a result), and fault tolerance (the system can survive the failure of one node at any point). This is a proven result.

This is correct.

Any distributed consensus system on the Internet must sacrifice one of these features.

This is potentially misleading. The FLP result shows that no system can provide those guarantees and reach consensus in bounded time. Real-world implementations of consensus like Paxos and Ripple however use probability to achieve safety, liveness and fault tolerance within a given time limit with very high likelihood.

If consensus is not achieved in this timeframe, the algorithm will retry and once again achieve consensus with very high likelihood and so on. In statistical terms, consensus will eventually be reached with probability 1, satisfying liveness under a probabilistic model. In practice, progress is usually made every round and two or more rounds are very rarely needed.

This means that distributed consensus systems like the Ripple network and Google’s Spanner database exist and can provide extremely high availability if configured correctly.

The existing Ripple/Stellar consensus algorithm is implemented in a way that favors fault tolerance and termination over safety.

This is incorrect. We have not reviewed Stellar’s modified version of Ripple consensus, but as far as the Ripple consensus algorithm is concerned, the protocol provides safety and fault tolerance assuming the validators are configured correctly. For a detailed proof, please see our consensus white paper.

This means it prioritizes ledger closes and availability over everyone actually agreeing on what the ledger is—thus opening up several potential risk scenarios.

This is incorrect. If a quorum cannot be reached, validators will retry until connectivity has been restored.

Issue 2: Provable correctness

Prof. David Mazières, head of Stanford’s Secure Computing Group, reviewed the Ripple/Stellar consensus system and reached the conclusion that the existing algorithm was unlikely to be safe under all circumstances.

We look forward to reading Prof. Mazières’ findings once they are published.

Based these findings, we decided to create a new consensus system with provable correctness.

As mentioned before, a proof of Ripple’s correctness is available in the form of the Ripple consensus white paper.

As Ripple Labs’ chief cryptographer and the original developer of Ripple consensus David Schwartz pointed out yesterday, there cannot be two conflicting majority sets without overlap. For bootstrapping with a small set of trusted validators, it is appropriate to use a crash-recovery fault model, meaning a simple majority such as three out of five is sufficient. In other words, it is impossible for the Ripple network to experience an unintentional ledger fork as Stellar’s did because our nodes require votes from a majority of validators. In the future, we will generally recommend a supermajority greater than two thirds to account for Byzantine faults (validators that act arbitrarily or maliciously), but otherwise the same concepts apply.

In either case, anyone wishing to join a specific set of mutually consenting validators in the Ripple topology can do so by configuring their local Ripple node appropriately. We recognize the immense task of building the world’s first global consensus graph. It is a hard problem, but not an impossible one. Like the transition from Arpanet to the distributed routing topology of the modern internet, it will require time, education and a great deal of caution. But thanks to our amazing partners and colleagues, we are ready to tackle this challenge.

The Ripple network and its distributed ledger have used the Ripple consensus protocol to operate reliably for two years and currently manage $ 1.4 million in daily volume. We continue to invest in scaling Ripple to support the world’s cross-border transactions with bank partners in the U.S. and Europe actively integrating today.

https://kinematec.de/wp-content/uploads/2019/10/kinematec_logo.png00christianhttps://kinematec.de/wp-content/uploads/2019/10/kinematec_logo.pngchristian2014-12-07 11:43:162015-01-12 07:32:59Why the Stellar Forking Issue Does Not Affect Ripple

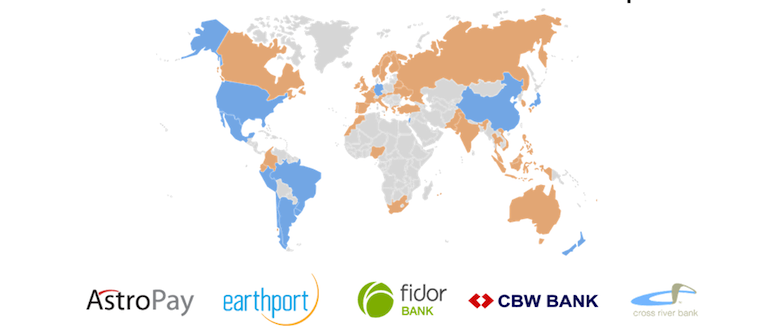

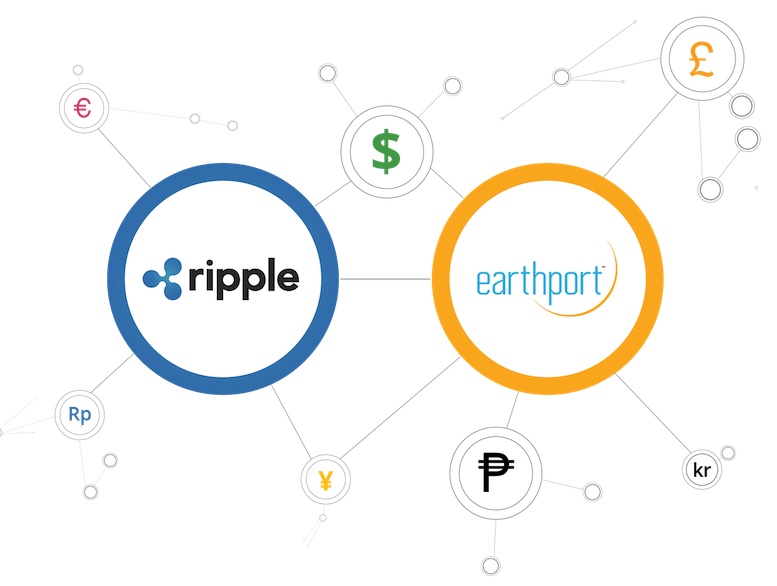

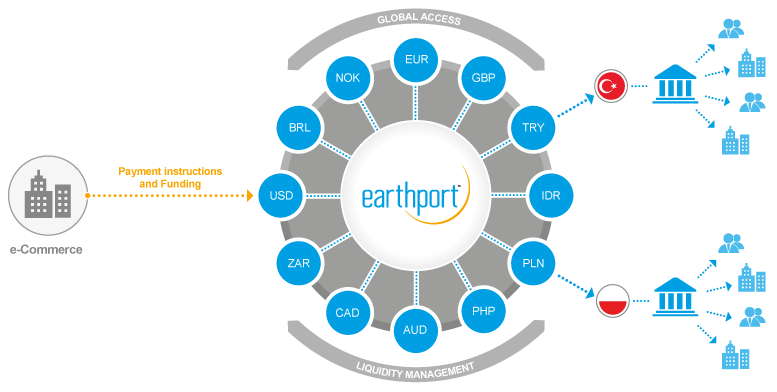

Ripple Labs is thrilled to announce a partnership with Earthport, a regulated financial institution whose cross-border platform represents the largest open network for global bank payments.

The London-based firm, which has offices in New York and Dubai, will integrate the Ripple protocol alongside its existing payments network. Through this global partnership, Earthport’s customers will be able to leverage Ripple’s friction-free cross-border payments solution and benefit from lower liquidity management costs, all while maintaining the robust standards of compliance that regulators expect.

“We constantly evaluate new technologies to reduce costs and delays associated with global bank payments for our clients, but require these innovations to meet our high, exacting standards for compliance,” said Hank Uberoi, CEO of Earthport. “Ripple is a new technology and, once integrated in our payments service could bring benefits in efficiency and speed to global transfers. Earthport will apply its existing compliance framework, rule sets and secure payments network to any Earthport clients transacting using the Ripple protocol.”

Growth in international trade, e-commerce, and demographic shifts in population have driven both corporate and consumer demand for faster, cost-efficient, reliable and transparent cross-border payment solutions.

Earthport is the largest open network for global bank payments, servicing businesses and financial institutions across 60 countries around the world. (Image: Earthport)

Ripple Labs is incredibly proud to have a partner at the forefront of the payments industry. Earthport was awarded the B2B Payments Innovation of the Year 2014 at the second annual FStech/Retail Systems Payments Awards. The company—which is listed on the Alternative Investment Market (AIM) on the London Stock Exchange and is authorised and regulated by the Financial Conduct Authority under the Payment Service Regulations 2009—services major institutional clients in over sixty countries.

“Traditional cross-border payments are inefficient today because both the technology and compliance frameworks underpinning them were built country by country decades ago,” said Chris Larsen, co-founder and CEO of Ripple Labs, the developer of the Ripple protocol. “The Earthport and Ripple partnership brings together the leading global payments and technology infrastructures to immediately transform and modernise the global payments industry.”

Earthport’s proven compliance platform provides an immense opportunity for international scalability given their expertise in navigating local regulations. For Ripple Labs, the partnership represents another major milestone as part of the company’s mission to develop and expand the Ripple network by plugging into the existing financial system.

https://kinematec.de/wp-content/uploads/2014/12/ripple-earthport-2.jpg586777christianhttps://kinematec.de/wp-content/uploads/2019/10/kinematec_logo.pngchristian2014-12-04 12:30:452015-01-12 07:33:12Ripple Labs and Earthport Announce Global Partnership

Superintendent Ben Lawsky hasn’t shied away from maintaining an open dialogue with the community.

While the early days of the web provide an intuitive roadmap for how the emergence of digital payment protocols and the ecosystem that surrounds them will evolve over time, there’s one defining difference between the evolving state of finance today and the Internet of the 80s: Regulations.

There’s a lot more at stake when transferring value versus information. It’s why finance is the most heavily regulated industry on the planet. It’s also why the internet-of-value has taken such a long time to materialize. The bar is just that much higher.

As these emerging technologies push us further into uncharted territory, navigating these regulatory waters has become a core component of our mission here at Ripple Labs. And as creators of an open source protocol, we’re committed to being transparent about that process. To provide insight on our perspective, we’re publishing our BitLicense comments (pdf), which we recently submitted to regulators.

Our position on regulations is straightforward. An effective regulatory framework opens the door to mainstream adoption. The goal is to provide necessary protections for end users without stifling innovation by burdening developers and small businesses. Instead, smart regulations can level the playing field, legitimize a burgeoning industry, and empower entrepreneurs.

But getting regulations right is an immense task. That’s why it’s pertinent that Ripple Labs works intimately with regulators, our numerous stakeholders, and the industry-at-large in helping to collectively shape the rules that will define the way forward.

BitLicense

It’s incredibly encouraging that the U.S. government appears up to the task with Superintendent Ben Lawsky of the New York State Department of Financial Services leading the way by maintaining an open dialogue and recently, drafting the first proposal of BitLicense, a set of rules that aim to bring clarity to how government officials and businesses deal with cryptocurrencies.

As the only U.S. regulator to step up to the plate—at both state and federal levels—Superintendent Lawsky should be commended for assuming this monumental responsibility. BitLicense elevates the industry as a whole, putting us in the same club as the big banks. Most of all, throughout Lawsky’s numerous interactions with the community—including his speech at Money20/20 in Las Vegas last month—it’s clear that New York’s first Superintendent of Financial Services not only comprehensively understands and respects the awesome potential of these new technologies but also what’s at stake.

Indeed, the implications of BitLicense will have far broader implications beyond the crypto-community, as Lawsky alluded to during his Vegas keynote, noting that his framework for Bitcoin regulations will eventually serve as a model for all regulated institutions. Along those lines, this isn’t merely about the future of Bitcoin or Ripple, it’s about the future of finance as a whole—one in which the lines between new technologies and the existing system continue to blur.

Again, for his fearless and influential leadership, Lawsky deserves to be commended. Even so, he could do more—especially if he and the rest of the state’s ruling body want New York to become a hub for technological innovation. Below is a summary of our comments and suggestions that we believe could help BitLicense reach its ultimate goals while still maintaining an environment that supports and fosters innovation and small businesses.

Reduce barriers of entry.New York should support developers who need the freedom to build. Costly compliance requirements create huge barriers of entry for small businesses. To accommodate innovation, we suggest a “registration regime” versus a “licensing regime” with a threshold for smaller firms, significantly reducing potential upfront costs and waiting around that often deters new businesses. This way, entrepreneurs can begin the regulatory process in good faith and start their business right away.

Create a level playing field. A key criticism of the initial BitLicense proposal is that it didn’t create a level playing field between cryptocurrencies and everyone else. There are arguments to be made why cryptocurrencies should be held to a higher standard their unique properties, but if that’s the case, those arguments need to be explicitly mapped out to each special feature individually relative to existing rulesets. With the initial draft, it’s often unclear why increased controls are being implemented only for cryptocurrencies.

The rules regarding information security is one example, which requires third-party code verification. In this case, rather than opting for a more organic approach, Lawsky went from 0-60 with these baseline regulations. While it may be true that this new rule could very well be a “coming attraction for all banks,” emerging technologies shouldn’t have to serve as the canary in the coal mine. If a new rule is believed to be beneficial to the public’s interests, it should be applied to all relevant parties on day one rather than arbitrarily to the new kids on the block. Otherwise, BitLicense undermines a sense of fairness by appearing to favor established interests.

The overall scope is too broad.Such is the nature of emerging technologies with few past precedents, they can be difficult to properly define, but even under that context, the way BitLicense defines these new technologies is far too general and vague. If the purpose of regulations is to provide clarity, the proposal as it currently exists risks further muddying the waters by leaving far too much to subjective interpretation. The first step then is to provide a concise definition of the technology at hand. The approach we prefer is to highlight the technology’s fundamental distinctions. In the case of virtual currencies, this is the first time we’ve seen assets exist in a digital context (as opposed to liabilities).

Beyond reaching consensus on a proper definition, we believe that limiting the scope of these new regulations requires a more balanced and organic approach to how we assess risk. It’s logical to focus on the risks added by new technologies, but it’s just as important to take into consideration existing risks that innovation helps to mitigate. In that sense, BitLicense should not only temper negative characteristics, but also foster and expand positive traits. In current form, the former is at times, over the top, while the latter is lacking.

The way forward

Overall, the development of BitLicense represents a huge step in the right direction, despite being imperfect as regulators and industry participants continue to work together toward a meaningful and mutually beneficial consensus.. That governments are dedicating these resources toward legitimizing new businesses is a huge stamp of approval for technologies that only a few short years ago didn’t even exist.

At Ripple Labs, we’re deeply cognizant of our responsibility to our partners, our community, and the industry, and we take great pride in participating in this ongoing process, one we believe will have a huge impact on our ability to deliver these breakthrough technologies to people around the world.

That last part is key. Even if the U.S. will, at times, lead the way, the scope and reach of Ripple and other digital payment protocols in general transcends borders. As such, our regulatory work extends to a global scale. Last Friday, our team submitted a letter to the Australian Parliament regarding the regulation of digital currencies, which is available on their website for download. (We are submission #21.) We are also in the process of engaging with other foreign regulators.

As always—as an ongoing conversation and an evolving process—we are open to any and all feedback. We look forward to hearing from you.

Wir können Cookies anfordern, die auf Ihrem Gerät eingestellt werden. Wir verwenden Cookies, um uns mitzuteilen, wenn Sie unsere Websites besuchen, wie Sie mit uns interagieren, Ihre Nutzererfahrung verbessern und Ihre Beziehung zu unserer Website anpassen.

Klicken Sie auf die verschiedenen Kategorienüberschriften, um mehr zu erfahren. Sie können auch einige Ihrer Einstellungen ändern. Beachten Sie, dass das Blockieren einiger Arten von Cookies Auswirkungen auf Ihre Erfahrung auf unseren Websites und auf die Dienste haben kann, die wir anbieten können.

Notwendige Website Cookies

Diese Cookies sind unbedingt erforderlich, um Ihnen die auf unserer Webseite verfügbaren Dienste und Funktionen zur Verfügung zu stellen.

Da diese Cookies für die auf unserer Webseite verfügbaren Dienste und Funktionen unbedingt erforderlich sind, hat die Ablehnung Auswirkungen auf die Funktionsweise unserer Webseite. Sie können Cookies jederzeit blockieren oder löschen, indem Sie Ihre Browsereinstellungen ändern und das Blockieren aller Cookies auf dieser Webseite erzwingen. Sie werden jedoch immer aufgefordert, Cookies zu akzeptieren / abzulehnen, wenn Sie unsere Website erneut besuchen.

Wir respektieren es voll und ganz, wenn Sie Cookies ablehnen möchten. Um zu vermeiden, dass Sie immer wieder nach Cookies gefragt werden, erlauben Sie uns bitte, einen Cookie für Ihre Einstellungen zu speichern. Sie können sich jederzeit abmelden oder andere Cookies zulassen, um unsere Dienste vollumfänglich nutzen zu können. Wenn Sie Cookies ablehnen, werden alle gesetzten Cookies auf unserer Domain entfernt.

Wir stellen Ihnen eine Liste der von Ihrem Computer auf unserer Domain gespeicherten Cookies zur Verfügung. Aus Sicherheitsgründen können wie Ihnen keine Cookies anzeigen, die von anderen Domains gespeichert werden. Diese können Sie in den Sicherheitseinstellungen Ihres Browsers einsehen.

Andere externe Dienste

Wir nutzen auch verschiedene externe Dienste wie Google Webfonts, Google Maps und externe Videoanbieter. Da diese Anbieter möglicherweise personenbezogene Daten von Ihnen speichern, können Sie diese hier deaktivieren. Bitte beachten Sie, dass eine Deaktivierung dieser Cookies die Funktionalität und das Aussehen unserer Webseite erheblich beeinträchtigen kann. Die Änderungen werden nach einem Neuladen der Seite wirksam.

Google Webfont Einstellungen:

Google Maps Einstellungen:

Google reCaptcha Einstellungen:

Vimeo und YouTube Einstellungen:

Datenschutzrichtlinie

Sie können unsere Cookies und Datenschutzeinstellungen im Detail in unseren Datenschutzrichtlinie nachlesen.