Every week, we’ll be offering a quick rundown of the most relevant news in finance and technology.

PayPal reached a valuation of $ 50 billion in its first day of trading on the Nasdaq as an independent company since its split from eBay (which had acquired PayPal back in 2002 for $ 1.5 billion). The market clearly sees payments as big business.

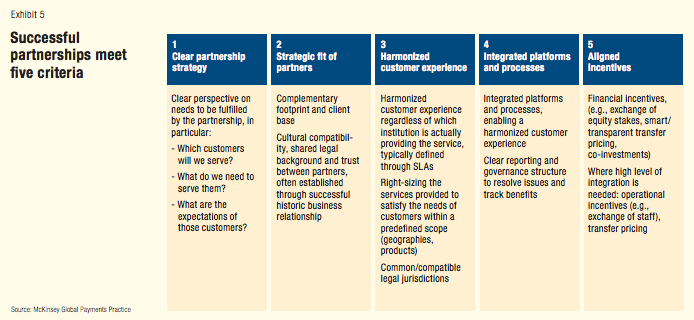

Successful partnership is possible, under the right circumstances. Source: McKinsey

In May, McKinsey released a report of their latest findings and advice on potential improvements in banking and payments.

The report points out that the threat of disintermediation looming over banks can be neutralized through the implementation of judicious partnerships and white-labeling of technological products that update aging infrastructure.

“Third-party platforms are making it possible for banks, non-bank financial institutions, payments processors and other organizations to customize cross-border services in ways that go beyond the options offered by traditional correspondent banking arrangements. Ripple Labs, having developed a real-time, cross-border open payment protocol based on recent cryptocurrency technologies, is an example of these new types of third-party platforms. Such innovators allow financial institutions to streamline and improve the service levels and costs of critical steps in the correspondent banking infrastructure, such as message routing and settlement. The speed at which new entrants are evolving, as shown by Ripple’s recent partnership announcement with Earthport, increases the potential for a significant disruption within the industry.”

https://kinematec.de/wp-content/uploads/2015/07/Screen-Shot-2015-07-20-at-9.05.52-AM.png320694christianhttps://kinematec.de/wp-content/uploads/2019/10/kinematec_logo.pngchristian2015-07-20 20:46:562015-07-29 16:29:12McKinsey: New Partnership Models in Transaction Banking

This is the first in a series of recommendations on who to follow in fintech social media. Stay tuned for more. #FintechFollowFriday

Financial technology is like a busy intersection in a huge city. Banking and finance runs east to west; from the venerable past into the unknown future. Traffic on that road isn’t as fast as it used to be, but it is dense and it stops for no one. Technology is the road that runs north to south; from the misty far-off territory of vision through the gridlock of development and finally into the gritty south industrial areas of implementation.

The place where they come together is packed, confusing, and it’s difficult to hear the message above the noise. These recommendations for who to follow on Twitter can help to establish a known traffic pattern; something that can be anticipated and followed if one gets lost.

Bradley Leimer is the head of innovation at Santander, and actually fills the elusive and difficult-to-define role of a fintech evangelist. His timeline is youthful, with clear interest in quantifying millennials as customers and viewing change as a constant as well as a good. He retweets often, but with an eye toward content curation. If you’re looking for thought leadership and a reading list, look no further.

Claire Cockerton is CEO and chairwoman of Entiq. Her timeline reflects a love for the possibilities of fintech and the good it can do in the world. She attends fintech events and often shares her thoughts or photos from them, so you can be there without being there, and she’s always involved in the Twitter fintech conversation.

Faisal Khan is the ultimate outside-insider. Khan is known as a consultant in fintech and one of the most accomplished answerer of questions on Quora. His timeline includes his blog posts, his podcasts, and his predictions about the payments market. If you like to think about what’s possible, follow Faisal Khan.

David Brear is the Chief Thinker at the Think Different Group, following up on a stint as director of digital banking at Gartner. Brear tweets an active and lively timeline about payments in the UK, as well as curating links on banking topics. He’s included in the @FinTechMafia and his contributions are often funny or sardonic. If you follow too many dormant or automated accounts, add Brear to wake things up.

Brian Knight is an associate director at the Center for Financial Markets at the Milken Institute. His timeline is varied, not all fintech all the time, but a mix of interest-piquing content that centers on finance and banking. Follow Knight if you enjoy fintech insights with a sprinkle of sarcasm and the occasional joke.

Brett King is a an influential voice in fintech that you can actually listen to— thanks to his #1 rated radio show, Breaking Banks. King is also an author, founder, and innovator. His timeline brooks no nonsense, and often aggregates important news from multiple sources. Follow King if you want to feel the pulse of fintech in your timeline every day and have access to some of the best podcasts on the subject of moving money.

Consumers are demanding faster payments in the UK. Photo: Flickr

This is part 1 of our 2-part interview series with Jeremy Light on the future of payments.

Real-time payments is the hottest topic in Europe if not globally, says Jeremy Light, a managing director at Accenture and payments industry expert.

When you think of influential authorities in the payments space, Jeremy instantly comes to mind. As head of Accenture Payment Services in Europe, Africa, and Latin America, Jeremy focuses on strategy, systems integration, and outsourcing.

A prolific thought leader, Jeremy regularly produces groundbreaking industry publications—such as his report, “Digital Payment Transformation”—and also maintains a blog. He was named Accenture’s Inventor of the Year 2015 after being awarded a mobile payments patent in 2014 along with his colleagues.

We recently caught up with Jeremy to get his take on the future of payments.

Ripple Labs: Everyone seems to be talking about real-time payments these days.

Jeremy Light: I would say probably the hottest topic in Europe if not globally is real-time payments. The Euro Banking Association (EBA) is focused on it. So is the European Central Bank (ECB). At the end of last year, the ECB issued a challenge to the banking industry in Europe—for them to develop a cohesive vision for building real-time payments infrastructure. They didn’t want to see disparate systems being set up around Europe that didn’t work together.

The EBA, which also performs a clearing function, set up a forum earlier this year across Europe to spark a discussion on real-time payments. But even without the extra nudge, we’re seeing progress in quite a few countries around the world, where banks are investigating how they can set up a real-time clearing system.

Last year, Finland issued a request for information (RFI), which described the national payment system there as quickly becoming obsolete. The Netherlands just announced that they’re going to set up real-time payments. Dutch banks plan to have real-time solutions set up by 2019. The EBA itself has just issued a blueprint for a pan-European instant payment infrastructure to be implemented from 2016 to 2018.

RL: So real-time is clearly on everyone’s minds. What are the biggest challenges moving forward? What are the major roadblocks?

Jeremy: Well, one major challenge is getting banks not only to adopt new technology and infrastructure, but also offer these products to their customers. Even now, there are banks around Europe that will say that their customers aren’t asking for real-time payments, that same day or next day payments is good enough.

RL:It kind of sounds like how Internet providers here in the US will say that their customers don’t want faster broadband speeds.

Jeremy: Right. Consider the UK, where we’ve had the Faster Payments System since 2008, which, by the way, is now growing very strongly. Despite having the capabilities all these years, banks haven’t really promoted or marketed real-time payments. That’s not necessarily the fault of the banks either. A lot of small businesses, until recently, have been more than content with same day payments. But I would say that in the past 18 months, there’s been a big shift in attitude. We can’t pinpoint exactly why, but customers are now demanding real-time payments.

As a result, those banks that can’t offer guaranteed real-time payments 24/7/365, they’re starting to notice that their customers are complaining because they see this service being offered by competitors. They see others doing it, that it’s possible and that it’s happening. So there’s definitely been a wave of change regarding expectations in the last year or so.

Here in the UK, we have a lot of upstart banks, called challenger banks, encouraged by the government’s drive to open up competition in the banking industry. These new banks realize that they have to offer a real-time payments proposition because if they don’t, they’ll be at a huge disadvantage.

RL: Which makes sense. Everything else in our world today is on demand. The Internet has wired us for instant gratification.

Exactly. We suspect that this shift in expectations is part of the rise of the digital age. People’s lives are governed by their smartphones and they experiences they get with Google, Amazon, and Apple, where everything is immediate and instantaneous. It’s pushing banks to change their stance.

Consider a scenario if a bank in Europe wanted to offer mobile payments because their customers are demanding it. If i send you a payment by mobile and you get a message—Jeremy just sent you $ 15.

But then you look at your bank account and you don’t see the money, it’s a problem. It becomes a source of uncertainty and anxiety. You don’t know when your money will arrive or even if it will arrive. And banks get that. They realize that they can’t offer mobile payments unless it’s in real-time and it’s a sea change that’s occurring across Europe.

So most banks, most countries are realizing that they need to implement these systems because if you think about it, it’s the natural progression. It’s evolution. Like you said, everyone is used to real-time in every other aspect of their lives. It just makes sense. When people send you an email, they want an instant response. If I ask you a question, I want an answer. I don’t want it tomorrow. I want it immediately.

RL: Given all of that, where do you think distributed ledgers fit into the equation?

It’s an interesting question. The distributed consensus ledger technology that Ripple offers and that blockchain technologies offer is coming along at just the right time when banks are looking at real-time payments. So there’s an immense amount of interest in what these innovations have to offer.

The caveat of course, is that these technologies still need to mature, particularly if we’re talking about the blockchain. If you look at Bitcoin, the maximum transactions right now is maybe around 3 or 4 per second. Then you look at Visa, which can process around 45,000 transactions per second. Bitcoin also isn’t technically real-time since it takes at least ten minutes to confirm a transaction. That isn’t to say these issues can’t be addressed, but right now, the technology hasn’t advanced yet and in terms of businesses offering real solutions, I haven’t seen any credible candidates. I don’t see it as this incredible technology that offers a solution for the immediate future. On the other hand, Ripple confirms transactions in seconds, which, I expect, is what banks are looking for.

RL: You make a great point about Visa. A lot of people will say, look, we can already do real-time with a centralized ledger and so they don’t understand the appeal of a distributed system.

Jeremy: That’s a key question. Why distributed ledgers? For one, a distributed solution enforces integrity and commonality versus one central ledger that everyone can access.

At the same time, central clearing and settlement is very efficient. Most clearing and settlement systems today can handle very high volume and they rarely have issues. Apart from very occasional hiccups, such as in the UK wire system last year, we haven’t really had issues regarding resilience.

Still, having these central, proprietary systems adds a lot of complexity and cost on the bank side. There’s a lot of different systems and these systems don’t interoperate with each other. This adds to operational issues and operational processes. So if we consider long term costs, a distributed ledger could conceivably be a better, more efficient solution, and there’s certainly the potential to do that. That’s why these technologies are so interesting for banks.

We’re still in the discovery phase around cryptotechnologies, distributed consensus ledgers. What will be intriguing to banks and financial institutions is to figure out how they can leverage the advantages of these innovations.

RL: Maybe this is an obvious questions, but what are the immediate benefits of real-time payments, given that customers are now demanding it as a service?

From a consumer point of view, there are two main advantages. The first is that you have real-time availability of funds. If I give my daughter a pound coin, she can immediately go and buy an ice cream, rather than in a few hours or the next morning. When you have real-time availability of funds, you’re much more flexible with what you can do.

The second advantage is the ability to provide a seamless customer experience. We’ve noticed that in the UK, if a bank has delays of even just 10 minutes, customers service call volumes go up significantly because someone was sent money, but when they go to the ATM, it hasn’t arrived yet.

People enjoy a sense of certainty. They like knowing that a job is done so they can forget about it. Today, because PayPal is connected to the Faster Payments System, you can move money between your bank account and PayPal account in real-time. The same goes for people who have accounts at different institutions, you can send money from one bank to another instantaneously. If you initiate a transaction and you see that it’s left one account and it hasn’t arrived in another, it’s painful.

That’s the customer proposition. It’s instant gratification, essentially cashless cash. If you give cash to someone, a $ 20 bill, that’s it. The transaction is done and you can move on. That’s the beauty of real-time payments.

And this is exactly the trend we are seeing. In the UK, we predict volumes on the Faster Payments System to double or triple in the next few years, and they are already at over a billion payments per year.

https://kinematec.de/wp-content/uploads/2015/07/london.jpg534800christianhttps://kinematec.de/wp-content/uploads/2019/10/kinematec_logo.pngchristian2015-07-16 20:42:512015-07-29 16:29:24Accenture’s Jeremy Light: The Future of Payments is Real-time

WiredMoney 2015 was held on July 8 at the British Museum in London, and as audiences have come to expect, the event attracted presenters and speakers from power players and new entrants to the world of finance.

Incumbents like Visa shared the stage with disruptors like Bitcoin, and Ripple Labs presented on the integration of legacy banking with distributed ledger technology. Newcomers to the industry showed off their proposals in the pitch sessions on the BBVA Ventures Startup Stage.

In this wealth of ideas and chorus of voices, there are a few highlights that stand out:

Ismail Ahmed, CEO and founder of WorldRemit, reasoned that cash is being replaced in much of the developing world by mobile phones; a process that brings historically unbanked people into the global economy for the first time.

Key quote: “45% of Kenya’s GDP flows through M-Pesa.”

Jonathan Vaux, executive director of innovations partnering at Visa Europe, represented his company as a friendly incumbent willing to partner with new players in financial technology and ready to adapt.

Key quote: “By working together we will succeed together.”

Peter Smith, CEO of Blockchain, presented on the concept of crowdsourced and provable identity that could be verifiable online. He proposed that this idea would be of particular use in countries without state-issued ID as well as in places where verification is costly or time-consuming.

Key quote: “Really at its core, Bitcoin is just an open access database that anyone can write to.”

Stefan Thomas, CTO of Ripple Labs, presented on the Internet of Value; the concept of integrating siloed financial institutions through Ripple’s partnership with banks to create a flat and completely connected payments world.

Key quote: “We believe this point in the future has finally come.”

The common thread that emerged in nearly every presentation was one of partnership; the necessity for new technology and legacy financial institutions to adopt and adapt to one another for the good of consumers all over the world.

Technologies are emerging that change irrevocably the way people all over the world identify themselves, move money, and make payments. As our own Stefan Thomas put it, this technology is not a future possibility; it is a current reality.

In its comprehensive report on the impact of emerging payment schemes, the message of the World Economic Forum (WEF) is clear—the industry must integrate legacy systems with new technologies in order the leverage the best of both worlds.

The report, which had a mandate to “explore the transformative potential of new entrants and innovations is the culmination of “extensive outreach and dialogue with the financial services community, innovation community, academia and a large number of financial technology startups” over the course of fifteen months.

As part of the report’s key findings for payments, the WEF concluded that the greatest potential for “decentralized and non-traditional payment schemes” such as distributed ledgers “may be to radically streamline the transfer of value, rather than as store of value”—thus creating “competitive pressure for the value transfer rails to become faster, cheaper and more borderless.”

In other words, decentralized payment schemes are all but declared heir apparent to legacy banking structures, allowing for the possibility that nontraditional payments networks could rival, disrupt, or be assimilated into the traditional financial network.

It does not frame this as a question of if, but as a series of predictions of who, when, and how. Specifically, the WEF foresees three possible outcomes outlined in the report:

Compete with an alternative network of financial providers

Facilitate alternative payment schemes as complements

Provide leaner, faster payment options within the existing network

In the first outcome, the two systems—the traditional and more modern financial systems—would remain disparate and have limited interaction with one another. This scenario is predicted to drive innovation, but possibly also expose consumers to unfamiliar risks.

The third outcome is considered the least likely—that incumbent institutions might transform their own payment and settlement systems, responding to competition with innovation to match. The financial industry is a slow-moving beast. Still, it appears many institutions get the picture. Banks like UBS, Deutsche Bank, and Citi are all betting big on fintech, launching so-called “innovation labs” around the world to experiment with new ideas.

But the WEF views the second outcome as the most productive, where the traditional banking structures adopt and integrate innovative technologies, fostering an ecosystem that combines the speed and ease of use of newer tech with the established identities of long-standing banks and improving the connectivity of historically siloed financial institutions.

The examples WEF provides (Fidor with Ripple and CIC with M-Pesa) represent this blending of establishment and disruptors offering “could be easily used for real-time payment and settlement between these institutions with no automated clearing house or correspondent banks required.”

This reality, the WEF suggests, represents the best of both worlds; the positioning and consumer confidence of legacy banking combined with the improved efficiency and compatibility with the real-time world that technologies can offer.

https://kinematec.de/wp-content/uploads/2015/07/WEF2-1024x768.jpg7681024christianhttps://kinematec.de/wp-content/uploads/2019/10/kinematec_logo.pngchristian2015-07-03 06:17:242015-07-29 16:29:36World Economic Forum Report: The Rise of Non-Traditional Payment Systems

An open marketplace has expanded both supply and demand for taxi services. Photo: Daniel Horacio Agostini

One unique feature of Ripple is the open nature of the network, which has numerous benefits for banks, market makers, regulators and ultimately consumers.

Given that the idea of an open value network is somewhat of a new paradigm, it’s worth going over just exactly what might mean for the payment ecosystem’s various stakeholders.

The benefit of an open network for banks

Managing information is pivotal for banks. As part of their daily operations, banks need to manage an endless flow of payment data, which also includes customer information. Not only do customers expect and demand this information to be kept private, regulators require it. Moreover, it’s important for banks to maintain confidentiality since transaction information—such as the volume or the currency—is considered competitive intelligence.

Throughout our numerous conversations with banks and financial institutions, a common question was whether or not an open network could facilitate both privacy and confidentiality. At first glance, “open” may seem concerning because banks naturally expect payment networks to be private.

In reality, Ripple satisfies both privacy and confidentiality. While transaction information on the ledger is public, payment information is not. It’s difficult for anyone to associate transaction information with any specific bank.

Finally, there are benefits to transparency, especially for cross-border (out-of-network) payments, which have traditionally been relatively opaque. End-to-end traceability will not only reduce risk and delays, it should also reduce the cost of compliance allowing banks to lower costs of fee-disclosures and regulatory reporting.

The benefit of an open network for market makers

The market for settling payments is huge. The heart of the issue is that it isn’t necessarily accessible. This undermines both efficiency and competition. Meanwhile, market makers already specialize in managing capital and the associated risks. As we’ve discussed previously, what Ripple does is essentially allow market makers to access what is essentially a marketplace for float, where market makers can compete to provide liquidity, which lowers costs for banks and businesses.

One way to understand the impact of expanding accessibility is to look at how Uber affected the marketplace for taxis. In San Francisco, the taxi market was about $ 140 million per year, according to Uber CEO Travis Kalanick. But Uber is already making three times that with revenues of $ 500 million per year. This means that competition doesn’t necessarily cannibalize existing revenue, it can help the entire pie grow much larger. In the case of Uber, by expanding the supply of drivers and offering a far better experience, many more customers decided to use taxi services rather than other modes of transportation, expanding the marketplace and eventually spurring on both innovation and competition.

The benefit of an open network for regulators

The role of regulators is to protect the welfare of any payment systems, primarily because payments can be used to finance activity that is deemed detrimental to society—such as crime and terrorism. As a result, being able to track payments is fundamental to regulators doing their job.

With the way things are today, it’s extremely difficult to monitor transaction activity given disparate systems, networks, and platforms plus the continued prevalence of physical cash. As a result, transaction monitoring is a highly manual and operationally intensive process, which means that regulators incur high costs simply to do their job or in some cases, they aren’t able to do their job as effectively as they would like.

For regulators, the open nature of Ripple provides further transparency and payment traceability, thereby reducing their costs while allowing them to do their jobs more effectively. If regulators and banks are able to automate compliance processes with Ripple, it reduces costs for everyone in the ecosystem.

In the end, however, the real winners are consumers, who benefit from a safer, more open, and competitive ecosystem that provides a platform for innovation, better access, and lower costs.

https://kinematec.de/wp-content/uploads/2015/07/taxi2.jpg533800christianhttps://kinematec.de/wp-content/uploads/2019/10/kinematec_logo.pngchristian2015-07-02 05:01:592015-07-29 16:29:45What an Open Network Means for Banks, Market Makers and Regulators

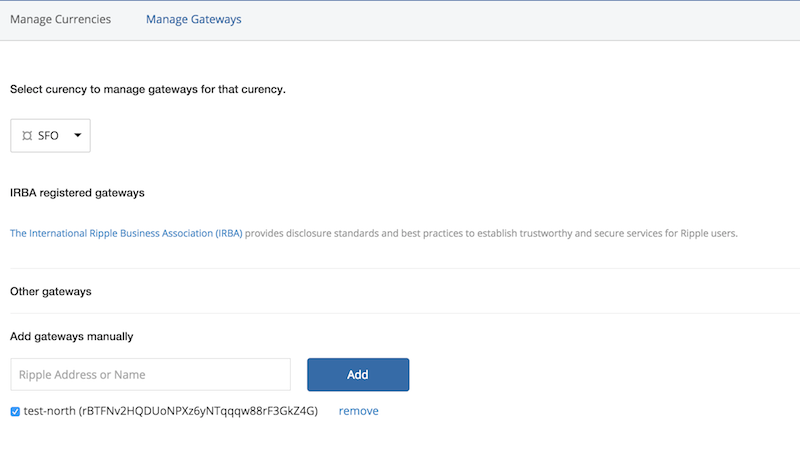

The Ripple ecosystem has many participants including gateways, market makers, and users—and we want to make it easier for you to customize the currencies and gateways that you access on Ripple Charts.

Although we have done our best to update the gateway list as often as possible, we are now launching a new feature that will allow you the ability to customize the currencies and gateways available in your Live Charts. The great news is that not only can you customize and add currencies and gateways to your hearts desire, you can also remove currencies and gateways that you never look at, enabling a more customized experience.

Customizing your currencies

Are you the type of person that might only look at 1 or 2 currencies on a regular basis? With the new dropdown customizations, you can now select the specific currencies that you would like to view.

Instructions:

1. Select on “Edit List” in the currency drop down.

2. You can also manage and deselect any currencies you aren’t interested in.

3. Return to the live chart to see your customized list!

Adding new currencies and gateways

Have you ever wanted to see Live Charts for a trading pair that wasn’t supported by the defaults provided by Ripple Charts? You can now add as many custom currencies and gateways as you choose.

Instructions:

1. Go back to the currency and gateway customization page and add your custom currency in the bottom field.

2. Once the currency is added, go to the “Manage Gateways” tab and select the custom currency you want to customize. Select or deselect any gateways that can be associated with the currency or add a custom gateway with the Ripple address or Ripple name.

Currency and gateway customization is only available on the ‘Live Chart’ page as of today. We plan to implement these customizations in the ‘Multi-Markets’ page within the next couple weeks.

Lastly, you’ll notice a slight facelift in the dropdowns as we’ve added new shiny logos for any gateways registered with the International Ripple Business Association (IRBA), a non-profit that sets standards and admits gateways based on their eligibility. Ripple Labs would like to promote best practices around compliance by featuring the logos of gateways that are members of IRBA and KYC their users. If you’re an IRBA member and not listed please contact our support team at . Also, please visit IRBA to become a member.

We hope these updates will provide benefit to those who’ve wanted some flexibility.

Over 75 people attended the Ripple Labs Tech Talk for understanding consensus—as part of our ongoing initiative to better educate the broader community about Ripple technology.

Approaching the talk from both a technical and broader industry perspective, Chief Cryptographer David Schwartz discussed the role of innovative banks, the early influences of Bitcoin, and provided a technical history and overview of the core processes underpinning the Ripple protocol.

Guests—who hailed from prominent tech firms, international financial institutions, and various universities—arrived early for a lively happy hour at the Ripple Labs headquarters in downtown San Francisco.

This was the second in the Ripple Labs series of Tech Talks.

In a lively Q&A segment, David answered a wide range of questions, from the technical—such as regarding the robustness of consensus—to the broad—including his take on bank innovation.

Since the beginning of recorded history, the process of standardization has set the stage for immense gains in collaboration, productivity, and innovation. Standards allow us to find collective harmony within a society that grows increasingly complex.

Naturally, the first standards were ways of measuring time and space—from the Mayan Calendar to King Henry I of England’s preferred unit of measurement in 1120 AD—the length of his arm—which he instituted as the “ell.”

While early standards often existed in part as a vehicle for increasing the prestige and power of rulers and regulators that created them, they would—as expectations evolved—become a source of individual empowerment. Following the French Revolution, a new system of measurement was promoted as “a way to erase the arbitrary nature of local rule,” writes Andrew Russell, author of the book, Open Standards and the Digital Age: History, Ideology, and Networks. The argument being—How could citizens truly be free, independent, and self-reliant if they weren’t able to make calculations and measurements on their own?

Indeed, it was broad standardization that paved the way for the Industrial Revolution. Interchangeable parts dramatically reduced costs, allowing for easy assembly of new goods, cheap repairs, and most of all, they reduced the time and skill required for workers. Or consider how those manufactured products are then shipped—likely by train. Prior to the standardization of the railroad gauge, cargo traveling between regions would have to be unloaded and moved to new trains because the distance between rails no longer matched the train’s wheels.

On the other end of the spectrum, the failure to enact proper standards isn’t just inefficient and costly, it can prove disastrous—such as in 1904, when a vicious fire broke out in Baltimore. New York, Philadelphia, and Washington, DC quickly sent support, but found their efforts to be in vain as their fire hoses weren’t compatible with local fire hydrants. The fire would burn for over 30 hours and destroy 2,500 buildings.

While the situation with today’s payment systems isn’t nearly as dangerous, the lack of a universal standard for transacting value is implicitly costly and serves as a persistent bottleneck toward true financial innovation.

In the U.S., the last time there was broad consensus on a new payments standard was with the creation of Automated Clearing House in the 1970s, an electronic system meant to replace paper checks. That system, which still essentially enables all domestic payments has, in four decades, remained relatively unchanged. The primary reason is that achieving consensus for new standards isn’t easy, especially in an industry as far-reaching and as fundamental to the economy as payments, where there are numerous and a wide range of constituents with incentives that don’t always align. So even as the Federal Reserve pushes for real-time payments, affecting actual change remains elusive, as the technology becomes increasingly antiquated.

While payment standards find themselves stuck in time, standards everywhere else have continued to evolve.

The latter half of the 20th century saw the rise of the concept of the open standard. While there’s no set definition for an open standard, there are a few commonly accepted properties, such as its availability to the general public while being unencumbered by patents.

Early manifestations of an open standard were physical, the quintessential embodiment being the creation of the shipping container. Conceptualized by Malcom McLean in the 1950s and later standardized by the U.S. Maritime Administration and the International Standards Organization in the 1960s, the shipping container became a universal standard for moving goods.

As the standard became widely accepted and used, shipping boomed and costs spiraled downward. In other words, the birth of globalization began with a standard. Such is the ubiquity of shipping containers today, they’re used for low-cost housing in the outskirts of Berlin, while serving as a beer garden in trendy parts of San Francisco.

As it turned out, open standards wouldn’t just facilitate transportation of goods, they’d also enable the efficient and cheap sharing of information through the internet.

Before the rise of open standards, it was physically impossible to connect different computers. Even if you could connect them, they each required proprietary information to understand one another. The creation of standards like Ethernet, TCP/IP, and HTML allowed an unprecedented level of interoperability and simplicity when it came to transporting data. “As we know in hindsight, each of these open standards created an explosion of innovation,” tech luminary Joi Ito wrote in 2009.

And Internet standards are still evolving—from Creative Commons for copyrighted material to OAuth for online authorization.

While open standards have liberated the movement of physical goods and digital information, moving dollars and cents has been disappointingly left behind. It’s one of the primary reasons that there are still 2.5 billion people who lack access to the global economy.

In many cases, serving the unserved starts with setting a standard. One place where that idea has taken hold is Peru, which has one of the lowest rates of inclusion in all of South America—8 out of 10 working adults don’t have access to proper financial services.

When the country initially investigated how to provide more people access, they assumed the problem was mostly technological. They soon discovered that technology was only a small piece of the pie and in order for financial inclusion efforts to truly move forward, regulators would have to create a clear regulatory framework that standardized new technologies while promoting innovation and competition.

The U.S. appears to be following suit. A recent report from the Federal Reserve highlighted four paths to modernizing the U.S. payment system. Tellingly, “option 2” of the report details the development of “protocols and standards for sending and receiving payments.”

That the U.S. central bank has acknowledged the potential for a new payments standard is momentous. Intelligently crafted standards create the potential for a common language, a universal platform where innovation and economics can flourish.

https://kinematec.de/wp-content/uploads/2015/03/2344752466_7857f1e1ae_b.jpg5881024christianhttps://kinematec.de/wp-content/uploads/2019/10/kinematec_logo.pngchristian2015-03-25 04:42:422015-04-08 10:30:24A Brief History of Standards

Wir können Cookies anfordern, die auf Ihrem Gerät eingestellt werden. Wir verwenden Cookies, um uns mitzuteilen, wenn Sie unsere Websites besuchen, wie Sie mit uns interagieren, Ihre Nutzererfahrung verbessern und Ihre Beziehung zu unserer Website anpassen.

Klicken Sie auf die verschiedenen Kategorienüberschriften, um mehr zu erfahren. Sie können auch einige Ihrer Einstellungen ändern. Beachten Sie, dass das Blockieren einiger Arten von Cookies Auswirkungen auf Ihre Erfahrung auf unseren Websites und auf die Dienste haben kann, die wir anbieten können.

Notwendige Website Cookies

Diese Cookies sind unbedingt erforderlich, um Ihnen die auf unserer Webseite verfügbaren Dienste und Funktionen zur Verfügung zu stellen.

Da diese Cookies für die auf unserer Webseite verfügbaren Dienste und Funktionen unbedingt erforderlich sind, hat die Ablehnung Auswirkungen auf die Funktionsweise unserer Webseite. Sie können Cookies jederzeit blockieren oder löschen, indem Sie Ihre Browsereinstellungen ändern und das Blockieren aller Cookies auf dieser Webseite erzwingen. Sie werden jedoch immer aufgefordert, Cookies zu akzeptieren / abzulehnen, wenn Sie unsere Website erneut besuchen.

Wir respektieren es voll und ganz, wenn Sie Cookies ablehnen möchten. Um zu vermeiden, dass Sie immer wieder nach Cookies gefragt werden, erlauben Sie uns bitte, einen Cookie für Ihre Einstellungen zu speichern. Sie können sich jederzeit abmelden oder andere Cookies zulassen, um unsere Dienste vollumfänglich nutzen zu können. Wenn Sie Cookies ablehnen, werden alle gesetzten Cookies auf unserer Domain entfernt.

Wir stellen Ihnen eine Liste der von Ihrem Computer auf unserer Domain gespeicherten Cookies zur Verfügung. Aus Sicherheitsgründen können wie Ihnen keine Cookies anzeigen, die von anderen Domains gespeichert werden. Diese können Sie in den Sicherheitseinstellungen Ihres Browsers einsehen.

Andere externe Dienste

Wir nutzen auch verschiedene externe Dienste wie Google Webfonts, Google Maps und externe Videoanbieter. Da diese Anbieter möglicherweise personenbezogene Daten von Ihnen speichern, können Sie diese hier deaktivieren. Bitte beachten Sie, dass eine Deaktivierung dieser Cookies die Funktionalität und das Aussehen unserer Webseite erheblich beeinträchtigen kann. Die Änderungen werden nach einem Neuladen der Seite wirksam.

Google Webfont Einstellungen:

Google Maps Einstellungen:

Google reCaptcha Einstellungen:

Vimeo und YouTube Einstellungen:

Datenschutzrichtlinie

Sie können unsere Cookies und Datenschutzeinstellungen im Detail in unseren Datenschutzrichtlinie nachlesen.