The guide comes with step-by-step, diagrammed explanations of typical gateway operations, a hefty list of precautions to make your gateway safer, and concrete examples of all the API calls you need to perform in order to get your gateway accounts set up and secure.

We’re proud of all the work we’ve done to make the business of running a gateway easier, but there’s still more work to do. If you have any questions, comments, or ideas, please send feedback to – or post it on our forums. We’d love to hear from you!

https://kinematec.de/wp-content/uploads/2019/10/kinematec_logo.png00christianhttps://kinematec.de/wp-content/uploads/2019/10/kinematec_logo.pngchristian2015-03-19 03:45:262015-04-08 10:36:04Do You Have What It Takes to Be a Gateway?

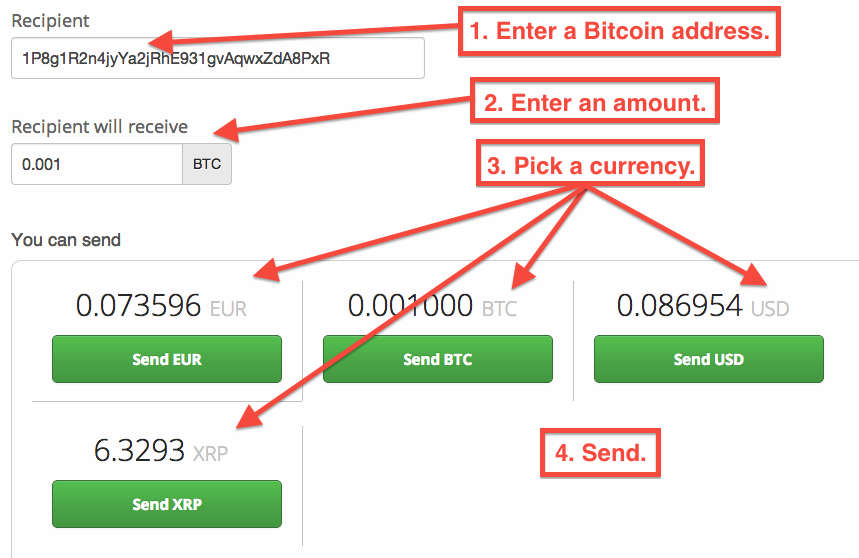

Ripple users can make payments to Bitcoin addresses directly from Ripple Trade.

Here’s how it works:

It’s that simple.

We call it a “Bitcoin Bridge” and it gives Ripple users access to the entire Bitcoin economy. Please note that payments through the Bitcoin Bridge may take a significant amount of time to be processed.

What Is The Bitcoin Bridge?

Ripple users can make a payment in any currency — dollars, euros, etc. — and the Bitcoin merchant will receive the payment in Bitcoins.

That’s good for Ripple users and it’s also good for Bitcoin merchants.

Thanks to the Bitcoin Bridge, all Bitcoin merchants now accept payments from Ripple users. More than 8,500 merchants are now available on the Ripple network:

The Bitcoin Bridge is a simple protocol that connects the Ripple and Bitcoin networks. When you send money from Ripple to a Bitcoin address, an organization running the bridge protocol facilitates the transactions.

The Bitcoin Bridge is operated by SnapSwap. Please reach out to SnapSwap for Bitcoin transaction details.

Currency Inclusive

Ripple was designed to be currency inclusive. Instead of promoting one currency or another, Ripple makes it easy to send payments in any currency and acts as a “universal translator” for money. The Bitcoin Bridge is one more step in Ripple’s mission to connect the disparate Internet payment systems into a single, shared, unified payment network, freely available and accessible to all.

Composed of over 25 prominent members in the payments space—including the likes of ACH, NACHA, and SWIFT—the IPFA promotes a grand vision for creating a global payments framework that facilitates interoperability and efficient cross-border payment processing.

“IPFA rules—when they are appropriately modified for Ripple—helps us create a complete, real-time, cross border payment system,” said Nilesh Dusane, director of business development at Ripple Labs.

“We’re very excited to join this network,” he said.

https://kinematec.de/wp-content/uploads/2015/03/Screen-Shot-2015-03-04-at-4.00.21-PM.png450800christianhttps://kinematec.de/wp-content/uploads/2019/10/kinematec_logo.pngchristian2015-03-05 03:54:072015-04-08 10:36:42Ripple Labs Joins International Payments Framework Association

Ripple Labs is honored to be recognized as the world’s fourth Most Innovative Company in Money for 2015 by Fast Company.

“We are thrilled to be named as one of the most innovative companies in money and to be included among such respected brands,” said Ripple Labs co-founder and CEO Chris Larsen.

The inclusion by Fast Company in its annual list builds on continuing recognition of the work we’re doing at Ripple Labs by the media and the industry at large.

“Our vision is to transform the world of finance in a way that benefits everyone from banks to governments to innovative developers to merchants, consumers and the financially underserved,” Larsen said. “It is gratifying to know that others share a desire for this change and recognize our work.”

Most Innovative Companies is Fast Company’s highly anticipated annual ranking of the world’s leading enterprises and rising newcomers that exemplify the best in business and innovation. You can check out the full list here:

https://kinematec.de/wp-content/uploads/2019/10/kinematec_logo.png00christianhttps://kinematec.de/wp-content/uploads/2019/10/kinematec_logo.pngchristian2015-02-09 21:05:332015-02-09 21:05:33Ripple Labs Makes Fast Company’s 2015 Most Innovative Company List

Chris Kanaan joined Ripple Labs two months ago to become the company’s VP of Engineering. The Yelp alum and Stanford grad is working closely with Ripple Labs CTO Stefan Thomas to oversee the engineering department, making sure teams are aligned with each other as well as the company’s product needs and vision. With headcount at nearly ninety, Chris’s arrival is timely, to say the least.

One reason the search took so long is because it was important to find someone who was not only qualified but was also the right cultural fit. Chris wholeheartedly checks both boxes and we’re all incredibly excited to have him on the team.

I sat down with him for a brief interview to learn more about the man named Kanaan and also to check in and see how his first eight weeks have been.

That’s when I came across Ripple. Something just clicked. It seemed like this was absolutely the next chapter in this movement. It took the best aspects of Bitcoin—like the ledger—but improved on the concept, such as the system for closing ledgers and the ability to support all currencies. I stared into the face of everyone on the “About” page on the company website, and I wondered, “Do I think these people can do it?” The answer was a resounding “Yes.”

Tell us about yourself!

Chris: After college, I moved to Kansas City, Missouri to take a very specific job doing 3D medical imaging at this huge 6,000 person multinational. I realized quickly that it wasn’t for me. They’d just paved their parking lot so I’d bring my skateboard in on the weekends to work. I’d code. Then I’d skateboard and think. And I just remember getting badgered by campus cops even though the entire lot was empty. It clearly wasn’t a good fit. I ended up getting an EMT license and working on an ambulance at night. I was on a rotational program and I ended up in London for a bit but the change of scenery didn’t help.

I’d always dreamed of moving to San Francisco—ever since I saw it for the first time as a little kid. I had this picture of me standing below the TransAmerica building in my dorm room. I thought it’d be the coolest place to be. So I got a one way ticket to the U.S. and stayed on a friend’s couch in Berkeley.

I ended up at a company called Quantcast after reading a Craigslist ad. They do real-time bidding for advertising. It was just a few people in a mostly empty room. Now it’s grown past 600. After Quantcast, I ended up at Yelp, where I worked for two years. I was an engineering manager, overseeing one team, then two. After Yelp, I took some time to be with my family and spent lots of quiet time exploring technologies I had been interested in, but hadn’t had time to investigate.

A few years back, I had mined some Bitcoin. I thought—This is so different from any of the other ideas I’ve heard. It wasn’t just another app. Plus, Bitcoin had this very mysterious character in Satoshi Nakamoto.

Fast forward to today, I had moved on from Bitcoin and forgotten my wallet. That’s when I came across Ripple. Something just clicked. It seemed like this was absolutely the next chapter in this movement. It took the best aspects of Bitcoin—like the ledger—but improved on the concept, such as the system for closing ledgers and the ability to support all currencies. I stared into the face of everyone on the “About” page on the company website, and I wondered, “Do I think these people can do it?” The answer was a resounding “Yes.”

I was lucky enough to join.

What are you working on at Ripple Labs?

Last year was about finding product market fit, and we figured out we needed to focus on liquidity first by integrating with the existing financial system before we can focus on end consumers. As a result, I’m very mindful of developing best practices to improve stability and our software development process, which will be key to becoming a true enterprise company.

What exactly are the responsibilities of a VP of Engineering?

I think Stefan (CTO at Ripple Labs) takes care of forward thinking and R&D. I complement him by growing the team and making sure everyone is on the same page—communicating well from across the aisle and also within teams. My job is to make sure we are all working together efficiently, productively, and most of all collectively. So I’m working closely with product, with all the engineering teams, and with HR and recruiting.

I’m also keeping tabs on what the business development team has up next for integration so we can adjust our product roadmap accordingly. It’s important that our products can scale, that they are applicable to a wide range of integration clients.

We also need to continue to maintain the engine that powers the entire network. I was very keen to meet everyone on the rippled team—where a lot of people are remote.

How’s it been so far?

I’ve been here eight weeks so far and it’s definitely been great. It’s excellent—not only what people have already done but also what we’re working on for the future.

It’s important that engineering is clearly focused now. Last year was grounded in explorations and experimentations. Now we have to drive that to completion if we want to have a strong, stable value network and to have partners using our technology across the world.

Chris Kanaan with Monica Long, VP of Marketing and Communications

How would you describe the team?

The way I view the rippled team, they are probably part of the top one percent of C++ developers. Each one individually was probably the smartest person at the previous company that they worked at. So it’s a big draw for them to work together—whereas at their previous job, their peers could only give them a rubber stamp because they couldn’t quite understand the scope and subtlety of their work. Now there is wide discussion across topics by compelling characters with diverse opinions. Above all, they’re working on a product that is completely fascinating.

In terms of the rest of the engineering team, they’re truly exceptional. It’s a nice mix of people who have worked in payments and finance as well as the startup world. So there’s good combination of experiences and the energy is apparent here. Everyone has a really good vibe, a buzz. Everyone is smiling. There’s an excitement but also this great attitude. As advertised, the culture has been humble and inclusive. And of course, as a young company, we have quite a bit of youth.

Can you tell us a little bit about who the real Chris Kanaan is?

I’m really interested in backpacking. The way I got into it—I had hiked the John Muir trail with a friend, in the winter. We didn’t see another human being for a month in these snowy mountains.

Toward the end of the trip, we saw two people. One woman was trying to set the speed record for the PCT. The other was a man named Scott, who was trying to do what he described as “the yo-yo,” a back and forth between Mexico and Canada on the PCT. I was just blown away.

The whole experience just opened my eyes. It was so cool, so surreal—not seeing anyone, then to see these people take it even further. I knew I had to try it myself one day. So my brother and I are planning to do it in 2020 or 2022.

Oh yeah, I also like to surf.

You’re just the quintessential Cali bro aren’t you?

I was actually born in the mountains overlooking Beirut. I moved here when I was nine.

Do you ever visit?

I go every couple of years. My dad’s side of the family is there so I always have to keep my Arabic up. But my mom is actually Swedish-American.

What about school, what did you study—given your wide range of interests?

I went to Stanford University and studied computer science. Later, I got a Master’s in sociology.

My advisor was on the board for Friendster and I got interested in understanding networks of people and representing that through code. I scraped websites of different companies to build a network of investors and C-level employees from different companies, looking for patterns in their social relationships. I wanted to see if you could use social distance to predict investment outcomes.

https://kinematec.de/wp-content/uploads/2015/01/ck-photo.jpg533800christianhttps://kinematec.de/wp-content/uploads/2019/10/kinematec_logo.pngchristian2015-01-29 19:49:322015-02-02 17:41:45Meet Chris Kanaan, VP of Engineering at Ripple Labs

The report follows calls for industry feedback in late 2013—which Ripple Labs participated in (letter, response)—during which the Federal Reserve acknowledged the payment system’s contribution to not only the country’s financial stability but also U.S. economic growth. The need to improve the nation’s underlying infrastructure had reached a critical juncture, the Fed concluded.

To put the significance of the Fed’s strategy report into context, this is the central bank’s first major initiative to upgrade the domestic payment system since the creation of ACH in the 1970s. This is a big deal—and the goal is clear.

The report’s executive summary overviews the current situation:

The Federal Reserve believes that the U.S. payment system is at a critical juncture in its evolution. Technology is rapidly changing many elements that support the payment process. High-speed data networks are becoming ubiquitous, computing devices are becoming more sophisticated and mobile, and information is increasingly processed in real time. These capabilities are changing the nature of commerce and end-user expectations for payment services.

Meanwhile, payment security and the protection of sensitive data, which are foundational to public confidence in any payment system, are challenged by dynamic, persistent and rapidly escalating threats. Finally, an increasing number of U.S. citizens and businesses routinely transfer value across borders and demand better payment options to swiftly and efficiently do so.

It’s also a call to arms:

Responses to the Federal Reserve’s 2013 Payment System Improvement – Public Consultation Paper (Consultation Paper) indicate broad agreement with the gaps, opportunities and desired outcomes discussed in that paper. Recent stakeholder dialogue has advanced significantly, and momentum toward common goals has increased.

Many payment stakeholders are now independently initiating actions to discuss payment system improvements with one another—especially the prospect of increasing end-to-end payment speed and security. We believe these developments illustrate a rare confluence of factors that create favorable conditions for change. Through this Strategies for Improving the U.S. Payment System paper, the Federal Reserve is calling on all stakeholders to seize this opportunity and join together to improve the payment system.

Of particular note are the potential solutions outlined by the report. Of the four solutions suggested, Ripple is the enabling technology described in option two (page 40). Ripple provides neutral payment infrastructure, and its users (banks, networks) set their own rules and governance in accordance with regulations set in their jurisdictions (e.g. the Fed in the U.S.).

Option 2: Facilitate direct clearing between financial institutions on public IP networks using protocols and standards for sending and receiving payments.

A distributed architecture for messaging between financial institutions over public IP networks has the potential to lower costs compared to clearing transactions over a hub-and-spoke network architecture. A central authority would establish common protocols for messaging standards, communication, security and logging transactions.

The Fed also made a statement about the design options it decided to exclude from further consideration, which included all proposals to evolve existing infrastructure such as ACH, wire transfers, and checks. They also decided to forego leveraging telecom infrastructure, a popular route in developing economies following the phenomenal success of M-Pesa.

The other options either involve leveraging the existing ATM/PIN debit infrastructure—which present numerous operational challenges such as “the high variability on implementation feasibility” and issue of “silos that often exist between the retail and commercial units of financial institutions”—or building new infrastructure from the ground up, which, while theoretically ideal as “a potential longer-term objective,” involves “potentially high cost.”

The Fed highlighted one of the primary weaknesses of the current status quo—that standards and protocols had failed to catch up to evolving needs as disparate networks and industry members failed to consistently reach consensus on new rulesets. The Fed pledged its commitment toward further industry coordination and cooperation to address this issue—which in our view underlines the unique advantage and responsibility of the central bank.

That’s also why we see Ripple technology as such a compelling solution within the components defined by the Fed that compose a payment system—technology, rules, risk management, and the messaging standard. As an efficient, inexpensive, ruleset-agnostic solution, Ripple provides the technological layer while the Fed and other industry members can play to their strengths and provide complementary components such as rulesets.

Ripple Labs designed the Ripple protocol as such because we believe that local jurisdictions are best suited to define their own standards in connecting fragmented payment networks given the complexity of financial regulation. By applying jurisdiction-specific rulesets on top of a common technical infrastructure like Ripple, the various national payment systems around the world would benefit from increased interoperability and a significant improvement in the speed and cost of cross border payments.

Having analyzed the Fed’s consultation papers over the past two years, we believe Ripple comprehensively achieves many of the desired outcomes outlined by the Fed (page 8-15) along with addressing many of the existing weaknesses highlighted (page 34).

In general, we applaud the Fed’s ongoing initiative to provide a safe, efficient, and broadly accessible payment network. Their active and inclusive approach provides us further confidence in the work we are doing at Ripple Labs.

https://kinematec.de/wp-content/uploads/2015/01/fed-strategies-ripple.png472800christianhttps://kinematec.de/wp-content/uploads/2019/10/kinematec_logo.pngchristian2015-01-27 04:24:262015-02-02 17:42:17The Fed’s Strategy for Improving the U.S. Payment System

In most cases, payments are included under a general framework for financial regulations. Yet the UK has taken a unique approach in designating a new regulator to build a more competitive, innovative and inclusive payment system.

Since the group will be fully operational in April 2015, the PSR called for industry input on its regulatory approach and initial priorities. Ripple Labs commends the PSR’s transparency, thoughtfulness, and inclusion in its call for input, and is grateful for the opportunity to submit a letter.

Our recommendations reflect ongoing discussions with regulators—such as our recent correspondence with New York Department of Financial Services (NYDFS) and the BitLicense proposal—and along those lines, represent our core perspective on regulations. That is, we believe the following four points to be essential to not only the PSR’s success, but regulatory frameworks in general:

Ensure regulations account for the new technologies that will be necessary for creating a more competitive, innovative, and inclusive payment system. Generally, existing regulations assume the use of a centralized operator. However, new technologies such as open protocols and distributed networks may not rely on a central operator. Regulators should ensure their rules account for technology with alternative governance models to best leverage their benefits in the payments system.

Enable startups and smaller companies to contribute to the payment system. We encourage a flexible regulatory framework that is inclusive of startups and smaller companies—typically the drivers of innovation. We commend both the PSR for recognizing this need in their proposals, as well as the NYDFS’ decision to include a two-year transitional operating license giving startups and small businesses an opportunity to compete with established players.

Take a holistic view of risk and consider the cumulative impact of regulations. New technologies present new risks, yet many of these risks are known and can be mitigated. Ripple Labs urges regulators to also consider the risk of continued reliance on antiquated infrastructure. These risks grow over time, are often underappreciated, and may have systemic consequences. Further, regulators should take a coordinated approach when implementing new rules, being mindful of their cumulative impact.

Consider how new infrastructure technology can minimize payment, operational, and systemic risks while improving anti-money laundering (AML) efforts. Novel approaches to infrastructure improvements can also go a long way in optimizing compliance capabilities and mitigating structural risks. In the case of distributed networks, the shared ledger lowers the cost of compliance by providing improved funds traceability and AML oversight.

In this case, we also included an overview of how Ripple benefits regulators, government agencies, and central banks. As an innovative approach to funds transfer, Ripple is an opportunity to improve today’s payment systems and minimize or even eliminate structural inefficiencies.

Unlike existing systems, Ripple is an Internet protocol-based technology, which means it is both neutral and also has the capacity to maintain a record of balances without a central counterparty. The result is a competitive market for funds exchange and delivery.

A payment system powered by Ripple has numerous benefits:

Reduces fragmentation and concentration; increases competition.

Enables fund traceability and transaction visibility.

Reduces systemic risk: no single point of failure.

Reduces the possibility of conflicts of interest as a neutral infrastructure layer.

Improves capital efficiency and liquidity management.

Decreases operational and settlement risk.

Enables new products and improved consumer experience.

Improves information security and reduces cyber threats.

In all, Ripple Labs supports and shares the PSR’s objectives of fostering a competitive, innovative, and inclusive payments systems. Indeed, we believe the Ripple protocol embodies many of the PSR’s goals. We look forward to continuing our proactive engagement with the PSR and other regulators in the future.

For a more in-depth overview of how Ripple Labs approaches regulations, you can view the entirety of our response to PSR CP14/1 here (PDF): Ripple Labs response to PSR

https://kinematec.de/wp-content/uploads/2015/01/regulations_and_compiance.png450800christianhttps://kinematec.de/wp-content/uploads/2019/10/kinematec_logo.pngchristian2015-01-22 04:16:362015-01-24 07:58:45Ripple: Benefits for Regulators and Payment Systems

Ripple Labs EVP of Business Development Patrick Griffin at Sibos 2013 in Dubai

Ripple Labs will be in Boston at the end of the month for Sibos (Sept. 29 – Oct. 2), the annual financial services conference hosted by SWIFT, where 7000 industry members and thought leaders will gather to contemplate and help shape the future of payments and trade.

Running concurrently throughout the conference is Innotribe program, a SWIFT initiative focused on innovation at the convergence of finance and technology—of which Ripple will play a prominent part. (Check out our interview with Kosta Peric, Innotribe co-founder and former Head of Innovation of SWIFT.)

Ripple Labs CEO and co-founder Chris Larsen will be presenting at the following sessions on Monday, September 29th:

Future of Money: The Rise of Cryptocurrencies (9:30AM ET)

Disruption: Cryptocurrencies (12:30PM ET)

If you’re interested in learning how Ripple is driving down cross-border transaction costs for banks like Fidor, please contact us at to schedule a meeting with a Ripple Labs representative.

To help accelerate the creation of strong, reliable, and compliant gateways, Ripple Labs will be providing XRP incentives and extended technical support for gateways that meet criteria considered to be critical for the success of a gateway.

Ripple Labs wants every gateway to achieve a gold standard in business planning, technical reliability and stability, regulatory compliance, and liquidity. The Ripple protocol enables the federation and interoperability of many independent payment systems.

As such, we’re actively developing the specifications for Gateway Services APIs and are eager to help gateways with implementation. In the meantime, here are some of the steps and assistance provided by Ripple Labs to help get your gateway to that point.

Gateway business plan development

Successful businesses start with a concept that can be concisely summarized and executed upon. To get things started on the right foot, here is a business plan template for gateways that is freely available. This plan was developed in consultation with new gateways that were exploring the business opportunities on Ripple, so it’s tailored to the needs of an early stage operator.

The template encourages you to carefully consider who your customer is and what value they’ll derive from your service. Simplifying their experience and making the deposit and withdrawal of assets frictionless is critical to driving volume and subsequent revenue.

Serious endeavors should contact Ripple Labs at to coordinate for possible assistance and business planning.

Gatewayd support

Gatewayd has been designed to make deploying a gateway as easy as possible.

It provides the basic functionality to link assets represented in the Ripple network to those held in the outside world. It includes a core database to track deposits and withdrawals and utilizes Ripple REST to issue assets to customer wallets.

Gatewayd plugins

If your gateway needs a custom deposit/withdrawal plugin for an external payment system (such as PayPal, AliPay, etc.), Ripple Labs may consider funding a bounty to create that plugin or build it for you. Plugins are custom pieces of code that are used to monitor and submit transactions to and from external payment systems so that gatewayd can take appropriate action. You can see examples of these kinds of plugins in the repos under gatewayd on GitHub.

Services implementation

Gateway Services APIs make gateways interoperable and provide straightforward calls that clients can use to route payments appropriately. Gateway Services rely on existing web standards like host-meta and webfinger, while making certain functions of the REST API more robust. Please contact us for assistance if you decide to implement these services at your gateway.

XRP for customers of KYC/AML compliant gateways

Ripple Labs may assist with customer acquisition by providing gateways with XRP that can be used to activate Ripple wallets of new accounts. Customers who provide a baseline level of KYC information may be eligible to receive XRP upon registration and making a deposit at your gateway.

Compliance resources

Ripple Labs regularly issues Gateway Bulletins as new features are released or on topics related to compliance and risk. Those bulletins are shared with the developer community including gateway operators and IRBA members. In addition to Gateway Bulletins, Ripple Labs publishes Compliance Resources that may be helpful for gateway operators in understanding local and global standards on KYC/AML policies, as well as opinions or guidance on virtual currency.

Since rules on KYC/AML policies and guidance on virtual currency vary by jurisdiction, gateways should obtain legal advice on how these rules apply to their business and country of operation. Be aware that regulatory standards are evolving rapidly. While Ripple Labs makes every effort to update the Gateway Bulletins and Compliance Resources regularly, gateways should seek legal advice and understand changes to regulation as it may vary based on geography and the products that you offer.

Generating liquidity

Ripple Labs understands that it may be difficult for new gateways to generate the liquidity needed to provide a compelling service to their customers. To do so, it is important to meet the aforementioned technical and compliance standards to have a popular, well-capitalized gateway. Transaction volume drives liquidity so Ripple Labs may facilitate introductions for operational gateways to market makers who can enable assets issued by your gateway to trade freely at competitive exchange rates.

Feedback is welcome

The Ripple protocol’s success will be largely determined by the ecosystem of gateways that are providing the onramps and off-ramps for value. As such, Ripple Labs continues to support gateway developers and entrepreneurs in their projects to build gateways.

We’d love to hear your feedback on what’s most useful and other tools that you’d like to see. We look forward to working alongside you to build the value web!

Ripple Labs is thrilled to have signed its first two U.S. banks to use the Ripple protocol for real-time, cross-border payments.

Cross River Bank, an independent transaction bank based in New Jersey, and CBW Bank, a century-old institution founded in Kansas, join Fidor Bank on the Ripple network, which continues to grow.

Both banks are excited to leverage the technology in order to provide greater efficiency and innovation to their customers.

“Our business customers expect banking to move at the speed of the Web, but with the security and confidence of the traditional financial system,” said Gilles Gade, president and CEO of Cross River Bank.

“Ripple will help make that a reality, enabling our customers to instantly transfer funds internationally while meeting all compliance requirements and payments rules. We are excited to be amongst the very first banks in the U.S. to deploy Ripple as a faster, more affordable and compliant payment rail for our customers.”

“Today’s banks offer the equivalent of 300-year-old paper ledgers converted to an electronic form – a digital skin on an antiquated transaction process,” said Suresh Ramamurthi, chairman and CTO of CBW Bank.

“Ripple addresses the structural problem of payments as IP-based settlement infrastructure that powers the exchange of any types of value. We’ll now be one of the first banks in the world to offer customers a reliable, compliant, safe and secure way to instantly send and receive money internationally. As part of our integration with Ripple, we are rolling out Yantra’s cross-border, transaction-specific compliance, risk-scoring, monitoring and risk management system.”

But these new partnerships aren’t just great for Cross River Bank and CBW Bank customers, it’s great for everyone in the U.S. and Europe by essentially opening up a corridor between ACH and SEPA. Any U.S. bank can now use Cross River or CBW Bank as a correspondent to move funds in real-time to any other institution in Europe via Germany-based Fidor.

The deals will also help expand liquidity and trade volume on the protocol and generally improve the network effects of the system—which will continue to make Ripple more attractive for both market makers and developers.

Ultimately, this announcement is the culmination of many months of hard work and further validation for the Ripple Labs vision. The most exciting part? This is only just the beginning.

https://kinematec.de/wp-content/uploads/2019/10/kinematec_logo.png00christianhttps://kinematec.de/wp-content/uploads/2019/10/kinematec_logo.pngchristian2015-01-12 11:47:032015-01-12 11:47:03Ripple Labs Signs First Two US Banks

Wir können Cookies anfordern, die auf Ihrem Gerät eingestellt werden. Wir verwenden Cookies, um uns mitzuteilen, wenn Sie unsere Websites besuchen, wie Sie mit uns interagieren, Ihre Nutzererfahrung verbessern und Ihre Beziehung zu unserer Website anpassen.

Klicken Sie auf die verschiedenen Kategorienüberschriften, um mehr zu erfahren. Sie können auch einige Ihrer Einstellungen ändern. Beachten Sie, dass das Blockieren einiger Arten von Cookies Auswirkungen auf Ihre Erfahrung auf unseren Websites und auf die Dienste haben kann, die wir anbieten können.

Notwendige Website Cookies

Diese Cookies sind unbedingt erforderlich, um Ihnen die auf unserer Webseite verfügbaren Dienste und Funktionen zur Verfügung zu stellen.

Da diese Cookies für die auf unserer Webseite verfügbaren Dienste und Funktionen unbedingt erforderlich sind, hat die Ablehnung Auswirkungen auf die Funktionsweise unserer Webseite. Sie können Cookies jederzeit blockieren oder löschen, indem Sie Ihre Browsereinstellungen ändern und das Blockieren aller Cookies auf dieser Webseite erzwingen. Sie werden jedoch immer aufgefordert, Cookies zu akzeptieren / abzulehnen, wenn Sie unsere Website erneut besuchen.

Wir respektieren es voll und ganz, wenn Sie Cookies ablehnen möchten. Um zu vermeiden, dass Sie immer wieder nach Cookies gefragt werden, erlauben Sie uns bitte, einen Cookie für Ihre Einstellungen zu speichern. Sie können sich jederzeit abmelden oder andere Cookies zulassen, um unsere Dienste vollumfänglich nutzen zu können. Wenn Sie Cookies ablehnen, werden alle gesetzten Cookies auf unserer Domain entfernt.

Wir stellen Ihnen eine Liste der von Ihrem Computer auf unserer Domain gespeicherten Cookies zur Verfügung. Aus Sicherheitsgründen können wie Ihnen keine Cookies anzeigen, die von anderen Domains gespeichert werden. Diese können Sie in den Sicherheitseinstellungen Ihres Browsers einsehen.

Andere externe Dienste

Wir nutzen auch verschiedene externe Dienste wie Google Webfonts, Google Maps und externe Videoanbieter. Da diese Anbieter möglicherweise personenbezogene Daten von Ihnen speichern, können Sie diese hier deaktivieren. Bitte beachten Sie, dass eine Deaktivierung dieser Cookies die Funktionalität und das Aussehen unserer Webseite erheblich beeinträchtigen kann. Die Änderungen werden nach einem Neuladen der Seite wirksam.

Google Webfont Einstellungen:

Google Maps Einstellungen:

Google reCaptcha Einstellungen:

Vimeo und YouTube Einstellungen:

Datenschutzrichtlinie

Sie können unsere Cookies und Datenschutzeinstellungen im Detail in unseren Datenschutzrichtlinie nachlesen.