For Ripple Labs, 2014 was the year in which we not only clarified our strategy for building the Internet of money but also made large strides in turning that vision into reality. From breakthrough partnerships to ecosystem expansion to the continued evolution of the underlying technology, 2014 has been a banner year. This is our year in review.

By the numbers

- Major partnership announcements: 4 (3 banks, 1 network)

- IRBA-certified Ripple gateways around the world: 16

- 24-hour network trade volume (all-time record): >$ 6.5 million

- 24-hour network trade volume (average, last 30 days): >$ 2 million

- Ripple network uptime: >99%

- Ripple ledger: 2 years old

- Ripple Labs headcount: 87 employees

Notable media coverage

The New York Times, The Wall Street Journal, Bloomberg, Bloomberg Businessweek, CNBC, USA Today, Fox Business, The Financial Times, Fortune, Institutional Investor, Forbes, Business Insider, International Business Times, Entrepreneur, VentureBeat, American Banker, TechCrunch, GigaOm, PandoDaily

Prominent industry research and reports

- Federal Reserve Bank of Boston: Current Policy Perspectives

- NACHA: Payments Innovation Alliance White Paper

- Mercator Advisory Group: Emerging Technologies Research

- Deloitte Center for Financial Services: 2015 Banking Outlook

- Bank of England Quarterly Bulletin: Money in the Modern Economy

- JWT Worldwide Trend Report: The Future of Payments & Currency

- Federal Reserve Bank of St. Louis: Dialogue With the Fed

- IIF Technology Showcase: Ripple Labs

- GSMA: The Evolution of Cross-Border Transfers

- OECD Working Paper: Currency Versus Trustless Transfer Technology

- The Nielsen Company: Lessons in Innovation Leadership

- The TAS Group: Real-Time Cross-Border Funds Settlement

- Aite Group: Challenging the Way Money Moves on the Internet

- Celent Group: The Disruptive Potential of Ledger-Based Technologies

The year we honed our vision

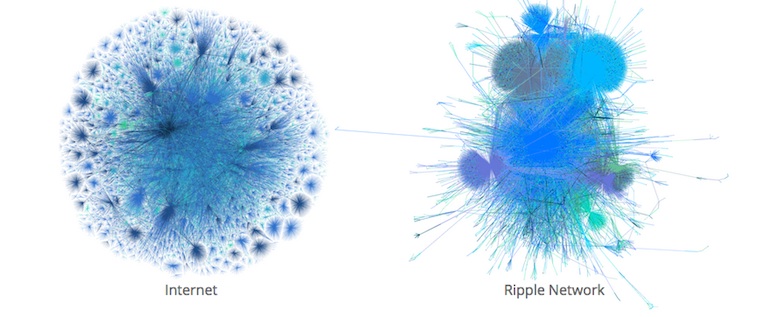

Navigating a startup working on brand new technology can be a perilous process. It can, at times, feel like you’re walking in the dark. But while it’s impossible to predict the future, we can look to the past for clues. In that regard, we see the state of payments tracking the history of the information web.

In September, Ripple Labs CTO Stefan Thomas published an op-ed in TechCrunch, outlining our vision for how the space will evolve, drawing parallels with the birth of the information web. Stefan breaks this evolution into three phases with each new phase building on the last.

The Infrastructure Phase: The original custodians of information on the Internet were universities and research facilities like CERN. While the network was already open and global in scope, it was still limited from a consumer perspective. In the case of payments, custodians of money, such as banks and governments, will lay the initial groundwork and plumbing for value transfer.

The Infrastructure Phase: The original custodians of information on the Internet were universities and research facilities like CERN. While the network was already open and global in scope, it was still limited from a consumer perspective. In the case of payments, custodians of money, such as banks and governments, will lay the initial groundwork and plumbing for value transfer.

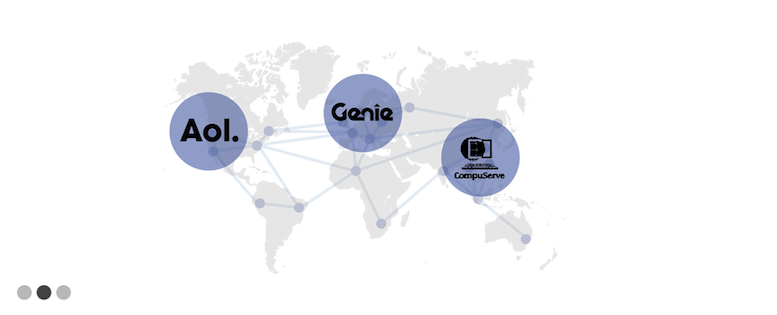

The Federation Phase: By the ‘80s, numerous services popped up to address increasing consumer demand, but these disparate networks originally weren’t interoperable. If you were on AOL, there wasn’t an easy way to connect with your friend on GEnie. This would be solved by the rise of common protocols like HTTP and SMTP that allowed networks to federate, bringing millions of consumers together all in one place. Similar to the Internet of the ‘80s, today’s payment networks aren’t yet federated, lacking a standardized protocol. Innovative services like Paypal, Alipay, and Venmo provide users with new features and convenience, but they also don’t interoperate. If you’re on Paypal, you can’t send your friend money if he or she is on Venmo.

The Federation Phase: By the ‘80s, numerous services popped up to address increasing consumer demand, but these disparate networks originally weren’t interoperable. If you were on AOL, there wasn’t an easy way to connect with your friend on GEnie. This would be solved by the rise of common protocols like HTTP and SMTP that allowed networks to federate, bringing millions of consumers together all in one place. Similar to the Internet of the ‘80s, today’s payment networks aren’t yet federated, lacking a standardized protocol. Innovative services like Paypal, Alipay, and Venmo provide users with new features and convenience, but they also don’t interoperate. If you’re on Paypal, you can’t send your friend money if he or she is on Venmo.

The Independent Value Phase: With everyone on the same network, it wasn’t long before developers and entrepreneurs started building services and businesses like Wikipedia, Google, and Facebook. What’s most exciting is that it’s impossible to predict what inventive, pioneering new industries will blossom. We believe that the same will hold true for the Internet of money.

The year we refined market fit and gained traction

Now that we had a better sense of where we wanted to go, we needed to figure out how to get there. The strategy that we ultimately defined reflects our ongoing commitment at Ripple Labs to create tools and technology that empower financial institutions, businesses, and ultimately developers.

We’re starting where Ripple provides the biggest impact for payments companies, app developers and ultimately consumers—the core. Skipping this essential developmental chapter to deliver these tools and technologies directly to consumers would be putting the cart before the horse. Partnerships with financial institutions establish a platform and market that others can build on higher up the application stack by first producing general utility and stability.

Just as the Internet of information required necessary groundwork before the likes of Peter Thiel and Mark Zuckerberg could change the world with PayPal and Facebook, the Internet of money requires a preliminary framework.

On the one hand, we need the web browser, the smartphone, and ubiquitous Internet access. On the other hand—in the case of moving money—we need liquidity, compliance and scalability. In place of universities and government institutions, we have financial institutions, which custody assets and already move trillions of dollars daily to solidify the foundation of the value web. Because of Ripple’s open nature, builders will be able to leverage the power and potential of the existing system in unimaginable ways. Where today’s systems are closed, tomorrow’s will be more open.

This is an admittedly challenging, painstaking, and laborious process, but fortunately, Ripple Labs—with the help of its supporters, partners, and community—made great headway in 2014.

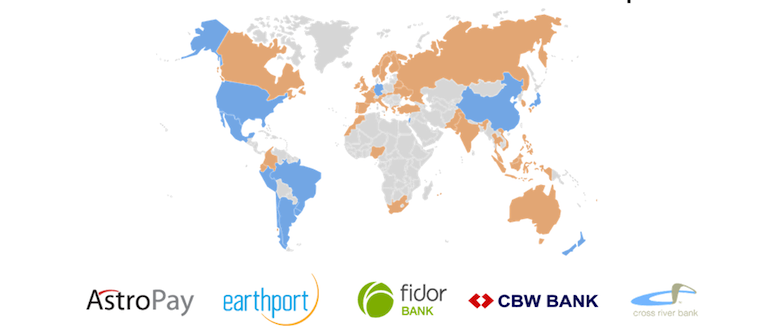

In May, we announced our partnership with Germany’s Fidor Bank, the first financial institution to integrate the Ripple protocol. Momentum kept building, leading up to Sibos, the annual financial services conference hosted by SWIFT.

To our pleasant surprise, Ripple was a persistent topic throughout the event, which attracted over 7,000 industry members. Where once potential partners worried about the reputational risk of integrating a brand new technology, now they were wondering how they could get started, perceiving innovation as a competitive advantage.

We got the sense that we were reaching a tipping point in terms of awareness within the financial community. This was particularly evident at a leadership workshop hosted by the World Economic Forum, which counted industry leaders like Deloitte, Barclays, and SWIFT. Again, many of the discussions centered around the Ripple protocol. During one presentation, a director of the Bill & Melinda Gates Foundation noted not only how Ripple could make cross-border payments more efficient but also how the technology could help address the ongoing issue of financial inclusion.

One week later, two U.S. banks, Cross River Bank and CBW Bank, joined Fidor in partnering with Ripple Labs. Then in November, we announced our global partnership with Earthport, the world’s largest payment network that services over 45 major banks in over 60 countries.

- The Ripple Protocol: A Deep Dive for Finance Professionals

- Fidor Bank AG: The First Bank to Use the Ripple Protocol

- Ripple Ecosystem Expands to 7 Countries in Latin America

- GBI Integration Allows Ripple Users to Trade, Send, and Spend Gold

- Ripple Labs Joins NACHA Alliance

- Ripple Labs Signs First Two US Banks

- Ripple Labs and Earthport Announce Global Partnership

The year the protocol matured

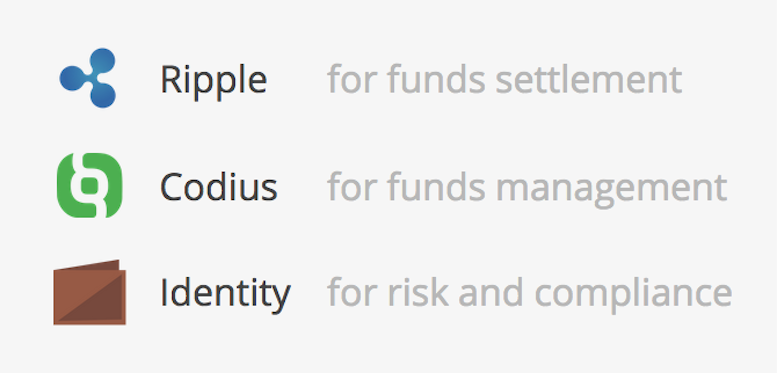

Fundamental to this strategy is the core technology that powers the Ripple protocol. In August, Ripple Labs released the consensus whitepaper, which describes the Ripple protocol’s consensus algorithm and properties.

Throughout 2014, the rippled team worked on improving stability, increasing rippled uptime to over 99 percent. The team also rolled out a series of new features and improvements including Account Freeze, transaction memos, and improvements to pathfinding. We’ve also completed development of features like Autobridging, which will be released in early 2015. Meanwhile, senior rippled developer Howard Hinnant completed his proposal relating to hashing infrastructure, which he submitted to the C++ Standards Body.

In all, the team made significant improvements to the stability, robustness, and value of the protocol.

- Ripple Consensus White Paper

- Introducing Offer Autobridging

- Powering Ripple and Helping Take C++ to the Next Level

- Types Don’t Know #, Howard Hinnant—CppCon 2014

The year the ecosystem grew and grew

The success we’ve experienced in 2014 in working with the existing industry was matched by grassroots efforts in our growing developer community. Today, developers and businesses have established Ripple gateways in every hemisphere. Along with the community, we also supported the establishment of the International Ripple Business Association, which provides best practice guidance to Ripple gateways and other businesses. The IRBA held its first officer elections this fall.

- How Ripple Labs supports gateways

- Meet Denis: Ripple’s First US Gateway Operator

- Meet Rafael Who Just Launched a Ripple Gateway in Brazil

- Pax Moneta: South Korea’s First Ripple Gateway

The year we expanded the scope of our tools

We realized early on this year that in order to achieve our mission of opening access to finance, we would need to build tools and platforms for business logic and identity management in addition to focusing on funds settlement.

Karen Gifford, chief compliance officer at Ripple Labs, summarized the opportunity for digital identity management in a Huffington Post op-ed. Today’s existing protocols for addressing the issue of identity simply come up short across the board. Not only is the way we deal with identity inefficient and costly, current procedures undermine both security and privacy by placing the onus on entities who aren’t security experts (like retailers and banks).

The longer term benefits may not yet be obvious, but it wouldn’t be far-fetched to think that a more versatile, portable identity system could empower individuals to own their own identities and help make financial services more available to the 2.5 billion people around the world who still lack access. When it comes to financial inclusion, proving one’s trustworthiness to service providers is the biggest obstacle.

In collaboration with MIT and dozens of prominent industry members, Ripple Labs contributed to the creation of the Windhover Principles, a set of principles and a framework for approaching new solutions for addressing digital identity, trust, and access to shared, open data.

- Huffington Post (Karen Gifford): When We Don’t Own Who We Are

- On the Road at G20: The Role of Identity in Financial Inclusion

- The Windhover Principles for Digital Identity, Trust and Data

- BitLicense: How Ripple Labs Approaches Regulations

The other key puzzle piece is smart contracts, which enables the application of rule sets and automated execution of those rules to funds transfer. In July, Stefan Thomas and team unveiled Codius, an open-source, smart contracts platform. From a broader perspective, it’s a framework for developing distributed applications, what we call “smart programs.” Stefan and team member Evan Schwartz presented Codius during a Tech Talk at the Around the World in Five Seconds event last month.

- Building Business Logic With Smart Contracts

- Codius Is Open Source

- Ripple Labs Tech Talk: An Introduction to Codius

Final thoughts

While Ripple Labs has made great headway in 2014, the hard work has only just begun. We look forward to building on the team’s and community’s successes for years to come.