The legislation enables banks to sell and store cryptocurrencies from January 1, 2020. Other providers will now require a German license.

The German parliament today passed a bill allowing banks to sell and store cryptocurrencies from next year.

The new legislation will come into force on 1 January 2020, and will require current custody providers and crypto exchanges operating in the country to take steps, before the end of the year, to apply for a German license.

The law will not only put Germany, the world’s fourth biggest economy, at the forefront of regulation in cryptocurrencies, but heralds a milestone in the adoption of cryptocurrencies.

“Germany leads the way in crypto regulation, for sure. This leads to institutional investors coming to Germany, as they want security and regulation,” Sven Hildebrandt, partner at German crypto consultancy DLC, told Decrypt. „Germany is well on its way to becoming a crypto-heaven.”

The bill was passed by the Bundestag, the lower house of the German Parliament, earlier this month, and approved by the upper house, the Bundesrat, today.

It amends a clause in the European Union’s Fourth Anti-Money Laundering Directive that currently prohibits banks from dealing directly in cryptocurrency. It allows them to legally sell and store cryptocurrencies, just as they do stocks and bonds, to retail as well as institutional investors.

At the same time, exchanges such as Binance and Kraken, and other digital asset custodians, will need to obtain a license from the German regulator, Bafin, if they wish to continue operating in Germany, said Hildebrandt.

In order to apply for this, companies will need a German legal entity with two directors operating in the country by the end of 2019. They also need to signal their intention to apply to Bafin for a license before 31 March 2020, and submit the application prior to 31 November 2020.

Digital asset custodians who have not established a legal identity in Germany before the end of the year will be deemed illegal by 2 January 2020, said Hildebrandt.

He said this leaves companies wishing to continue provide services in Germany with three options: to set up a German company before the end of this year, and then apply for a licence; to work with a cryptocurrency custodian who is licensed in Germany, or to work with a licence provider, which can offer a “complex but clever“ solution.

Companies have already begun to act on the new German law. Crypto Storage, a subsidiary of Swiss financial services provider, Crypto Finance announced plans to open an office in Frankfurt today.

Hildebrandt said that the new law will be a major breakthrough. “If you can hold [cryptocurrencies] in your bank account, that is massive for adoption,” he said. “I believe that this will act as a role model for all the other laws that will be coming into force Europe wide. Germany is driving crypto adoption forward and wants to play a leading role in Europe as well. One of the key challenges is keeping private keys safe.”

“I believe the biggest impact will be on exchanges such as BitStamp, Kraken and Binance, who are looking deeply into this,” he added.

The proposals were also greeted with enthusiasm by Germany’s banking community.

But consumer protection watchdogs have warned that it could mean banks could aggressively pitching cryptocurrencies to uneducated customers, putting them at risk.

https://kinematec.de/wp-content/uploads/2019/11/börlin.png499834christianhttps://kinematec.de/wp-content/uploads/2019/10/kinematec_logo.pngchristian2019-11-29 16:40:332019-12-06 12:43:15New law makes Germany “crypto heaven”

“The stock-to-flow approach originating in commodity-market analysis serves to quantify the ‘hardness’ of an asset. Applied to Bitcoin, an unusually strong correlation emerges between the market value of this cryptocurrency and the ratio between existing stockpiles of Bitcoin (‘stock’) and new supply (‘flow’),” they say.

Es hat ein wenig gedauert, bis das Bundesfinanzministerium das Urteil des Europäischen Gerichtshofs zur bundesdeutschen Tatsache gemacht hat. Aber nun ist es soweit. Sorgen, dass es irgendwie doch noch zu einer Verumsatzsteuerung von Bitcoin-Verkäufen kommt, haben sich damit endgültig erledigt.

Nachdem wir vor etwa zwei Wochen die Meldung hatten, dass das Finanzamt Bonn-Innenstadt versucht, von einem Bitcoin-Unternehmer die Umsatzsteuer für den Verkauf von Bitcoin zu verlangen, hat dies für ein gewisses Entsetzen in der Szene gesorgt. Unbestätigten Berichten zufolge hat dies zu Schlaflosigkeit unter Bitcoin-Tradern geführt und in einem extremen Fall sogar eine Psychose ausgelös. Manch ein Trader begann, sich wegen der potenziell hohen Umsatzsteuernachforderung um seine wirtschaftsliche Existenz zu fürchten. Mit ausgelöst wurde die Unruhe etwa durch Berichte des Steuerberaters Rüdiger Quermann sowie des Rechtsanwalts István Cocron.

Experten wie der Steuerberater Diplom-Kaufmann Christian Densch aus Essen, der als „Kryptotaxpert“ Gastgeber einer beliebten Facebook-Gruppe ist, haben von Anfang an energisch darauf hingewiesen, dass hier unnötig Panik verbreitet wird. Die Forderungen des Finanzamtes Bonn-Innenstadt seien in keinster Weise zu halten. Sie seien auch kein Ausfluss einer wie auch immer gearteten Verschwörung der Finanzämter, die nun versuchten, Bitcoin kaputt zu machen und die Bitcoin-Trader zu ruinieren, sondern lediglich das Ergebnis einer gewissen Trägheit der Behörden. Es sei weder notwendig, sich Sorgen zu machen, noch angebracht, Ängste zu schüren oder gar das persönliche Armageddon zu verkünden.

Wie sich bald darauf zeigte, hat der Steuerberater Christian Densch recht. Ihm gelang es im persönlichen Gespräch und einem darauf folgenden E-Mail-Verkehr, eine zur Veröffentlichung freigegebene Einschätzung von Dr. Christian Hufen zu bekommen. Dr. Hufen ist Persönlicher Referent des Parlamentarischen Staatssekretärs des Bundesministeriums für Finanzen, Dr. Michael Meister. Er schreibt, dass sich Kryptotaxperts „Vermutung, dass der Umtausch von Bitcoins in andere Währungen unter eine Umsatzsteuerbefreiung fällt, bestätigt“ hat. Es gilt die Entscheidung des Europäischen Gerichtshofes im Fall Hedqvist. „Danach handelt es sich bei dem Umtausch konventioneller (gesetzlicher) Währungen in Einheiten der virtuellen Währung ‚Bitcoin‘ und umgekehrt um eine Dienstleistung gegen Entgelt, die unter die Steuerbefreiung nach Art. 135 Abs. 1 Buchst. e der Richtlinie 2006/112/EG des Rates vom 28. November 2006 (sog. EU-Mehrwertsteuer-Systemrichtlinie, MwStSystRL) fällt.“

Der Steuerberater Densch hat noch einige weitere Fragen gestellt – etwa zum Mining oder zur steuerlichen Handhabung von Zahlungen mit Bitcoin – auf die der Persönliche Referent interessante, und im großen und ganzen auch erfreuliche Antworten gibt. Aber dazu ein andermal mehr. Hier sollte man feststellen, dass das Thema der Umsatzsteuer für den Verkauf von Bitcoins vom Tisch war.

Ein Schreiben des Bundesfinanzministeriums an die obersten Finanzbehörden der Länder vom 27. Februar, das auf der Webseite des Ministeriums veröffentlicht ist, bestätigt nun auch gegenüber den Behörden die Anwendung des Urteils des EuGH und bestätigt den Inhalt der E-Mail, die “Kryptotaxpert” bereits am 21.02.2018 auf seiner Seite veröffentlicht hat. Beim Umtausch von Bitcoin in Euro handelt es sich um eine „steuerbare sonstige Leistung, die im Rahmen einer richtlinienkonformen Gesetzesauslegung nach § 4 Nr. 8 Buchst. b UStG umsatzsteuerfrei ist.“ Die Grundsätze dieser Anordnung seien in allen offenen Fällen anzuwenden. Wer also sich noch irgendwie von der Umsatzsteuer bedroht fühlt, kann nun offiziell aufatmen.

Warum aber hat das Bonner Finanzamt nun trotz all dem einen Umsatzsteuerbescheid erlassen? Die Antwort darauf dürfte einen interessanten Einblick darin geben, wie deutsche Behörden zu arbeiten verpflichtet sind. Die Hauptsachgebietsleiterin Betriebsprüfung und Gewerbesteuer beim Finanzamt Bonn-Innenstadt verwies im Rahmen eines Telefonats mit Herrn Densch darauf, dass ohne Anwendungsschreiben der vorgesetzten Behörde ein EuGH Urteil nicht unmittelbar durch das Finanzamt umgesetzt werden darf. Unglücklicherweise orientierte sich die Verwaltungsmeinung noch an der Auffassung des BMF die Umsätze mit Bitcoin unterliegen der Umsatzsteuer. Das Finanzamt Bonn-Innenstadt hatte somit keine andere Wahl, als den mißliebigen Bescheid zu erlassen, auch wenn es sich selbst im klaren war, dass dieser nicht rechtens sein kann.

Es wäre interessant, wenn sich der Betroffene auch einmal zu Wort melden würde, bei der Aufregung, die um dieses Thema erzeugt wurde, dürfte ihm das ja nicht entgangen sein.

https://kinematec.de/wp-content/uploads/2018/03/dreamstime_xxl_109915247.jpg15362048christianhttps://kinematec.de/wp-content/uploads/2019/10/kinematec_logo.pngchristian2018-03-04 08:55:362018-03-04 08:55:36Nun ist es offiziell: Die Umsatzsteuer auf Kryptowährungen ist endgültig vom Tisch

On May 6, 2010, the stock market collapsed. The Dow Jones Industrial Average, Nasdaq Composite and S&P 500 all nose-dived, losing around 9% of their value. A trillion dollars was wiped off the value of companies. Within 20 minutes, most of the losses had been regained and within 36 minutes and the event was over. Whatever hit the economy that day had nothing to do with the true state of America’s finances.

An investigation into the Flash Crash focused on the algorithms used by high-frequency traders, companies that rapidly buy and sell stocks as their computer programs spot small price differences across the market. Five years later, police arrested Navinder Singh Sarao, a small trader who was believed to have made more than $40 million during the crash. Trading from his small house in London, he was alleged to have used a computer program to rapidly place sell orders to drive down prices, cancel the orders before the trades went through, then buy the stocks at the lower rate. He wasn’t the only one to make money that day, but his actions were enough to help move the market.

Prior to Bitcoin, the process for maintaining the transaction ledger remained effectively unchanged since the Medici developed double entry accounting in the 14th century. The Medici process of accounting required banks…

Bitcoin is going to do to banks what email did the post office and Amazon did to retail. Understandably those at the center of the financial system are concerned.

The banker’s mantra of “blockchain not bitcoin” has caught fire on Wall Street – everybody loves blockchain, they may not know what it is, but they love it! Jamie Dimon, CEO of JPMorgan, hates Bitcoin, but loves blockchain, Goldman Sachs CEO, Lloyd Blankfein, has embraced blockchain while he is warming to Bitcoin. Admittedly, I suffered from the same love affair with blockchain. As an early adopter of Bitcoin I still had feelings for the currency, but for a period of time I was infatuated with blockchain.

https://kinematec.de/wp-content/uploads/2017/10/bitcoin-2007769_1280.jpg8981280christianhttps://kinematec.de/wp-content/uploads/2019/10/kinematec_logo.pngchristian2017-10-24 08:19:232017-11-04 10:20:54Why Bitcoin Matters More Than Blockchain

Blockchains are beginning to turn green. This post describes some of the IC3 research in this direction.

The glorious view from our windows at Cornell Tech takes in 432 Park Avenue, the tallest residential building in the world. This tower is a monument to many things. Above all, for a student of Financial systems, it epitomizes ways to store wealth with breathtaking waste. (Fittingly, it was inspired by a wastepaper basket, shown to the right.) Buildings like it are sprouting up around NYC as investment vehicles for the ultra-wealthy, and their owners don’t actually live much in them. 432 Park and its ilk are essentially hollow vaults.

Something similar can be said for Bitcoin. As a concept and technological inspiration, Bitcoin is a marvelous thing. And unquestionably like 432 Park, it does see legitimate and valuable uses (and some shady ones). As a currency, though, Bitcoin serves in no small degree as a wasteful and ecologically damaging way for people to park their money.

There are a number of ways to substantiate this claim. One is in terms of its electricity consumption. Estimates vary, but it is likely that the Bitcoin network consumes roughly as much electricity as a nuclear reactor, about 1/3 of the entire electricity consumption of the entire country of Ireland. (See our back-of-the-envelope calculations in the blog notes.) To view this in another light, a recent IC3 paper estimated the cost-per-confirmed transaction at as much as $6.20 in capital costs and electricity. (Transaction rates have been rising, and today the figure is substantially lower, but still high.) That’s $6.20 in resources per transaction to move money between accounts in the same system.

Bitcoin proponents argue that this is simply the cost of decentralization. A credit-card network doesn’t provide the pseudonymity, freedom from government interference, portability, and other features of Bitcoin, so it isn’t comparable. This is true. But it isn’t a law of nature that a system like Bitcoin should be so resource-intensive. Researchers at IC3 believe that the many benefits of Bitcoin can be had without the waste. In a few papers released over the past month or so, we’ve outlined three different approaches to the development of greener alternatives:

PieceWork is a tweak to standard cryptocurrency PoWs that enables recycling of mining effort.

Resource-Efficient Mining (REM) repurposes innately useful workloads for mining effort. It relies on use of a trusted hardware technology called Intel SGX.

Snow White is the Proof-of-Stake system with rigorous security guarantees.

PieceWork: Recycling PoWs

If we can’t reduce waste at the source, why not recycle? That’s the premise of the first, and simplest idea, called PieceWork. Piecework involves a slight modification to the standard Proof-of-Work (PoW) construction, decomposing it into two layers. One layer produces small PoWs called puzzlets that play a critical role in the mining process and can also, as we shall show, serve useful non-mining purposes.

Consider a standard cryptocurrency, abstracting away into a single value X the details of what gets hashed into a PoW (transactions, the previous block, etc.). A miner’s task then is is simply to search for an input (“nonce”) n∈N for which

H(X, n) ≤ Z,

where Z is a threshold representing the difficulty of the PoW.

To decompose a PoW into two layers, we instead construct it as follows:

H(X, n) = Fout (X, Fin (X, n; rin ), rout ),

where rin = H0(r) and rout = H1(r) for distinct hash functions H0, H1 and a secret value r. (These two values are a technical requirement to prevent what are called block withholding attacks. See the blog notes.)

A valid solution is a value n such that

Fin (∙, n, ∙) < Zin and Fout (∙, n, ∙) < Zout.

To solve this puzzle or PoW, a miner must first find an n such that Fin (∙, n, ∙) < Zin. This inner-puzzle is what we call a puzzlet. To solve the whole PoW, a miner must find a puzzlet solution. The puzzlet solution must additionally satisfy Fout (… n…) < Zout, meaning that a miner must in general come up with many puzzlet solutions to solve the PoW as a whole. By setting Zin + Zout = Z, one obtains a PoW with the same difficulty as that in (1).

What’s the benefit of this two-layered structure? A puzzlet, i.e., the task of finding a solution n to Fin (∙, n ,∙) < Zin, can be outsourced by a miner or mining pool operator to a worker, and put to any of several non-cryptocurrency goals. DoS prevention for TLS is one example. TLS requires computationally intensive crypto operations from a server to set up connections. Thus it’s a natural target for DoS attacks, prompting the idea of requiring clients to solve PoWs if a server comes under attack, an idea now floated in an IETF proposal. These PoWs used for DoS mitigation can themselves be puzzlets. The effect is that the server becomes a mining pool operator, and its clients become workers. And a DoS attacker effectively showers the victim HTTPS server with cryptocurrency. (Of course, a server can also dispense puzzlets and make money even when it’s not under attack…) Other examples of puzzlet uses are spam prevention (the original PoW goal proposed by Dwork and Naor), MicroMint, and Tor relay payments.

In summary, PieceWork requires only a small modification to standard cryptocurrency PoWs. It turns them into dual-use computational problems and recycle wasted mining effort. How much recycling it can feasibly accomplish is an open research question. PieceWork benefits from a number of previous, related ideas. Our short paper on it can be found here. PieceWork will be presented in April at BITCOIN 2017.

Resource-Efficient Mining (REM): Using Innately Useful Work as Mining Effort

A very different approach to minimizing waste is embraced in our second project, a system called REM. Rather than relying on hash-based PoWs, it makes use of an entirely different type of PoW, in which the W, i.e., the work, is useful. We call this concept Proof of Useful Work (PoUW).

Of course, traditional PoWs have several useful properties, prime among them the ease with which solutions can be verified. Most workloads don’t have this property. To enable verification of work on arbitrary useful workloads, REM relies on a new technology: Intel SGX.

Intel’s new SGX (Software Guard eXtensions) trusted execution environment technology. In a nutshell, SGX enables the execution of an application in a hardware-protected environment, called an enclave, that is isolated from the operating system and other applications. It thus protects the application against tampering by even the owner of the machine on which it’s running. SGX also enables generation of an attestation that proves to a remote party that a particular application was running in an enclave. SGX is already supported in many recent-model Intel CPUs.

As a good way to see how SGX can facilitate mining, it’s worth discussing an elegant mining scheme proposed by Intel called PoET (Proof of Elapsed Time). The idea behind PoET is simple. If miners use SGX, then they can be forced to use only a sanctioned piece of mining software that simulates PoWs. Standard PoWs have solution times that are exponentially distributed. A PoET client can thus sample a solution time from an exponential distribution, simply sit idle until this time elapses, and then wake up with a block in hand. The first client to awake gets to publish its block. An SGX attestation proves to others in the system that the client idled as it should have.

PoET has several nice features. Foremost among them is the fact that (at first glance) it’s virtually energy-waste-free. Clients idle instead of hashing. Block solution times can be tuned to mimic those of a standard mining regime, like Bitcoin or Ethereum mining. Thus PoET can effectively be plugged into such schemes. It is also relatively egalitarian in that it achieves precisely one vote per CPU. PoET, though, has two technical challenges. We call these the broken chips and stale chips problems.

First, the broken chips problem. SGX security is imperfect and, as with any trusted hardware, it’s to be expected that a well-resourced adversary can break it. Thus, it’s to be expected that some SGX CPUs will be broken. In the basic PoET scheme, a broken chip has devastating effect, as it enables a miner to simulate a zero mining times and win every consensus round, i.e., publish all blocks. Intel has proposed a statistical testing regime to detect breaks, but details aren’t published and formal foundations are needed for a good analysis.

REM faces the same challenge. In REM, we have developed a rigorous statistical testing regime with formal foundations and shown analytically and empirically that it is highly effective: It can strictly limit the gains of adversaries that have broken chips while minimizing incorrect rejection of blocks from honest miners.

The stale chips problem is more subtle. Our economic analysis shows that in many practical settings in PoET and related systems, it will be advantageous for a miner to buy old (“stale”) SGX CPUs and cobble them together into “farms” that mine cheaply. Such farms reinstate a fraction of the waste that PoET is trying to avoid to begin with. This is where REM’s Proof of Useful Work (PoUW) approach comes into play. In a nutshell, with PoUW, miners run whatever workloads they consider to be useful—protein-folding computations and ML classification algorithms are a couple of examples considered in our work. Miners can prove that they did work on these problems using SGX. The probability of a miner mining a block is proportional to the amount of work she does. Thus, REM turns otherwise useful work into mining effort. Making PoUW work is technically challenging. It requires that workloads be themselves compiled and instrumented using SGX to prove correctness, an innovation of independent interest introduced in REM.

The biggest objection lodged against SGX-based mining is the fact that it places Intel in charge, undermining the decentralization at the heart of permissionless ledgers. Of course, Intel is already a trust anchor. But we’d view this another way, and characterize REM and PoET as partially decentralized. You can read about REM here, in a paper under submission.

Snow White: Proof of Stake with Rigorous Security Guarantees

Our final approach to reducing cryptocurrency waste is one both proposed and studied by many projects in the cryptocurrency community since the inception of Bitcoin. This idea is called proof of stake, and revolves around the basic premise that rather than mining simulating a lottery where your chance of finding a block is proportional to computing power, mining simulates a lottery where your chance of finding a block is proportional to the number of coins (or “stake”) you have in the system.

A key roadblock to the adoption and deployment of proof of stake systems involves questions around the security guarantees that they provide. This continues to be an ongoing source of controversy and debate in the community, with sources like the Bitcoin Wiki claiming that “Proof of Stake alone is considered to an unworkable consensus mechanism” and efforts like Ethereum’s Casper project studying questions of how to design a maximally useful and relevant proof of stake protocol for the next generation of cryptocurrencies.

Despite its potential shortfalls, we believe proof of stake represents a critical new development and direction in both the blockchain and distributed consensus fields. With this in mind, we set out to apply previous work by Rafael Pass (an IC3 member) and others, in which a model for analyzing and proving consistency, chain growth, and restrictions on adversarial chain impact for proof of work blockchains was developed.

To more accurately model the nature of blockchain distributed consensus, and the implication of network delays, we propose a new model for consensus called the sleepy model. This model more accurately mimics the operation and naturally captures the design of permissionless blockchains. In the sleepy model, a user (node or miner) can leave or join the protocol at will. This is modeled by (non-crashed) users in the protocol being given the ability to “sleep”, or go offline and rejoin the network at some unspecified later date with unmodified original state. The key question then becomes how can we design a useful consensus protocol in the sleepy model, when at least half of all online nodes (or stake) is honestly following the protocol?

The guarantees of consistency and availability are rigorously defined in this new model, more accurately capturing the guarantees users expect from blockchain protocols. The analogues of proof-of-work style guarantees like chain growth (availability) and chain quality (integrity) are also discussed. We believe this new class of consensus protocols in the “sleepy” model represents one of the fundamental contributions of blockchains to the distributed consensus space. Neither the asynchronous, partially synchronous, or synchronous models, in either a permissioned or permissionless setting, prove sufficient to model or reason about these new consensus protocols or the probabilistic and often economic guarantees they provide.

To that end, we are working on two protocols proven in the Sleepy model: Sleepy and Snow White.

Sleepy is a simple protocol intended to achieve the guarantees of chain quality, chain growth, and consistency/agreement with 51% of online nodes being honest. This protocol is intended for deployment in a permissioned context, and assumes stake assigned or instantiated by some trusted source. This makes Sleepy ideal for bankchains or other permissioned deployments, in which the set of stakeholders is known a priori but the blockchain guarantees of robust, auditable distributed consensus remain desirable. Every second, every member of the committee is eligible to “mine” a new block in the system, which involves a standard block mining solution with a public source of entropy as the nonce. Standard difficulty adjustments retarget the block interval to a desired target, as in Bitcoin and Ethereum today. The challenges of choosing an appropriate, ungameable mining function and source of entropy are tackled in the work, and proof is given that no committee member can manipulate the protocol to their advantage.

Snow White, on the other hand, is an extension of Sleepy intended to provide the same rigorous blockchain-derived guarantees in a permissionless setting, such as in the deployment of a public cryptocurrency. Obviously, this is substantially more difficult: choosing appropriate committee members for the block lottery, as well as ensuring that no coalition of these committee members (of bounded size) can game the protocol for more than a negligible advantage, are highly nontrivial. The resulting protocol is actually quite simple: each step, a committee mines as in Sleepy, with a shared source of entropy h0. With sufficiently many bits of entropy in h0 and an appropriately selected committee weighted on stake, it is possible to prove the desired result of chain quality, growth, and consistency in the Sleepy model. Choosing both the committee and h0 such that no adversary or non-majority coalition of adversaries gain substantial advantage by deviating from the protocol is the key to the construction and concrete parameters of the protocol, which are discussed further in our full publication.

Sleepy and Snow White represent the first rigorously justified and proven blockchain consensus protocols in both the permissioned and permissionless proof of stake space. It is our belief that the rigorous proofs of security are valuable as both theoretical efforts and to guide protocol development and deployment. Both the proof and concrete parameterization of these protocols are highly non obvious, and while heuristic protocols designed elsewhere in the community (with only informal justification) may operate in a similar manner to Sleepy, there is no guarantee that subtle network-level, timing, committee / stake poisoning, and other attacks are not present in these protocols. In our work, we assume an optimal adversary with ability to delay network messages up to some arbitrary time, a very strong notion of attacker that makes our protocols the most rigorous conceived in the space thusfar.

You can read about the papers in prepublication manuscripts we have uploaded for release on ePrint: Snow White, Sleepy. Further conference or journal publications with implementation details of these systems, full proofs, simulation results, and experimental comparisons to existing cryptocurrencies are currently in development. We hope to share more exciting news about these new protocols soon.

[It is worth noting that our willingness to assume that the majority of online coins are honestly following the protocol is an assumption that `has been challenged <https://blog.ethereum.org/2016/12/06/history-casper-chapter-1/>`_ by the Ethereum foundation. We do not necessarily agree with these criticisms or model; we believe that the ε-Nash equilibrium achievable in *Snow White is sufficient for the design of a robust, decentralized coin. Nonetheless, we believe developing and proving protocols secure in this context is valuable: both as the most natural model for private blockchain deployments, and to illuminate common pitfalls in proof of stake protocol design that may lead to attacks in naive protocols. We look forward to a full specification of Ethereum’s Casper, and to comparing both its assumptions and attack surface with that of Snow White.

There are many estimates of the electricity consumption of the Bitcoin network, but we don’t find them convincing. For example, this widely cited one derives an upper bound of 10 GW (in 2014!). As we’ll see from a simple calculation below, that would imply that miners were losing huge amounts of money. So here’s our crack at a crude estimate.

Using the technique in this paper, to obtain a lower bound on electricity consumption, let’s take the Antminer S9 to represent the state of the art in mining rigs. It consumes 0.098 W/GH. The current mining rate of the Bitcoin network is about 3,330,000 TH/s. Thus, were all miners using Antminer S9s, the electricity consumption of the network would be about 326 MW. (Of course, many miners are probably using less efficient rigs, so this is a loose lower bound.)

To obtain an upper bound on electricity consumption, assume that miners are rational, i.e., won’t mine if it causes them to lose money. At the current price of about $1000 / BTC, given a 12.5 BTC mining reward and block production rate of about 6 blocks per hour, the global mining reward per hour is about $72,500. A common, extremely cheap form of electricity used by miners is Chinese hydroelectric power; the very low end of the levelized cost of such electricity is $0.02 / kWh. Thus rational miners will consume no more than 3.625 GW of electricity. (Of course, this estimate disregards the capital costs of mining, and is therefore probably a quite loose upper bound.)

Taking the log-average of these two bounds yields an estimate of 1.075 GW, about the output of a single unit in a nuclear power station. Ireland’s average electricity consumption is about 3.25 GW (as derived from this 2013 figure).

Again, this is a crude estimate, but we believe it’s probably within a factor of 2 of the real one.

Why use rin and rout in PieceWork?

It is possible to outsource mining with the standard cryptocurrency PoW H(X,n) ≤ Z, simply by declaring a puzzlet to be the problem of finding an n such that H(X,n) ≤ Z_{easy}, for some Z_{easy} > Z. In other words, a worker can be asked to find a solution to a PoW easier than the target. But with some probability, a solution to H(X,n) ≤ Z_{easy} will also be a solution to H(X,n) ≤ Z, i.e., will solve the outsourcing miner’s PoW.

The problem with this approach is that a malicious worker can mount a block withholding attack. If it happens to find a solution to H(X,n) ≤ Z, it can simply not submit it. Or it can demand a bribe from the outsourcer. Use of rin and rout conceals from a worker whether or not a puzzlet solution is also a solution to the global PoW, preventing such attacks.

One thought on “The Bitcoin Group #40 – New York Regulation Week 2 – Ethereum Pre-Sale – Coinye – Ecuador”. thebitcoingroup. 10/08/2014 at 04:20 · Antworten. Hinterlasse eine Antwort Antworten abbrechen. ethereum – Google Blogsuche

https://kinematec.de/wp-content/uploads/2019/10/kinematec_logo.png00christianhttps://kinematec.de/wp-content/uploads/2019/10/kinematec_logo.pngchristian2014-12-29 11:53:472015-01-12 07:26:04The Bitcoin Group #40 – New York Regulation Week 2 – Ethereum …

Presented by Stephan Tual, CCO. Companion Document: https://medium.com/@ethereumproject/4790bf5f7743 Ethereum is a platform that makes it possible for any de… Categories : Kryptowährungen. Bookmark the … ethereum – Google Blogsuche

One of the latest ideas that has come to recently achieve some prominence in parts of the Bitcoin community is the line of thinking that has been described by both myself and others as “Bitcoin dominance maximalism” or just “Bitcoin maximalism” for short – essentially, the idea that an environment of multiple competing cryptocurrencies is undesirable, that it is wrong to launch “yet another coin”, and that it is both righteous and inevitable that the Bitcoin currency comes to take a monopoly position in the cryptocurrency scene. Note that this is distinct from a simple desire to support Bitcoin and make it better; such motivations are unquestionably beneficial and I personally continue to contribute to Bitcoin regularly via my python library pybitcointools. Rather, it is a stance that building something on Bitcoin is the only correct way to do things, and that doing anything else is unethical (see this post for a rather hostile example). Bitcoin maximalists often use “network effects” as an argument, and claim that it is futile to fight against them. However, is this ideology actually such a good thing for the cryptocurrency community? And is its core claim, that network effects are a powerful force strongly favoring the eventual dominance of already established currencies, really correct, and even if it is, does that argument actually lead where its adherents think it leads?

The Technicals

First, an introduction to the technical strategies at hand. In general, there are three approaches to creating a new crypto protocol:

Build on Bitcoin the blockchain, but not Bitcoin the currency (metacoins, eg. most features of Counterparty)

Build on Bitcoin the currency, but not Bitcoin the blockchain (sidechains)

Create a completely standalone platform

Meta-protocols are relatively simple to describe: they are protocols that assign a secondary meaning to certain kinds of specially formatted Bitcoin transactions, and the current state of the meta-protocol can be determined by scanning the blockchain for valid metacoin transactions and sequentially processing the valid ones. The earliest meta-protocol to exist was Mastercoin; Counterparty is a newer one. Meta-protocols make it much quicker to develop a new protocol, and allow protocols to benefit directly from Bitcoin’s blockchain security, although at a high cost: meta-protocols are not compatible with light client protocols, so the only efficient way to use a meta-protocol is via a trusted intermediary.

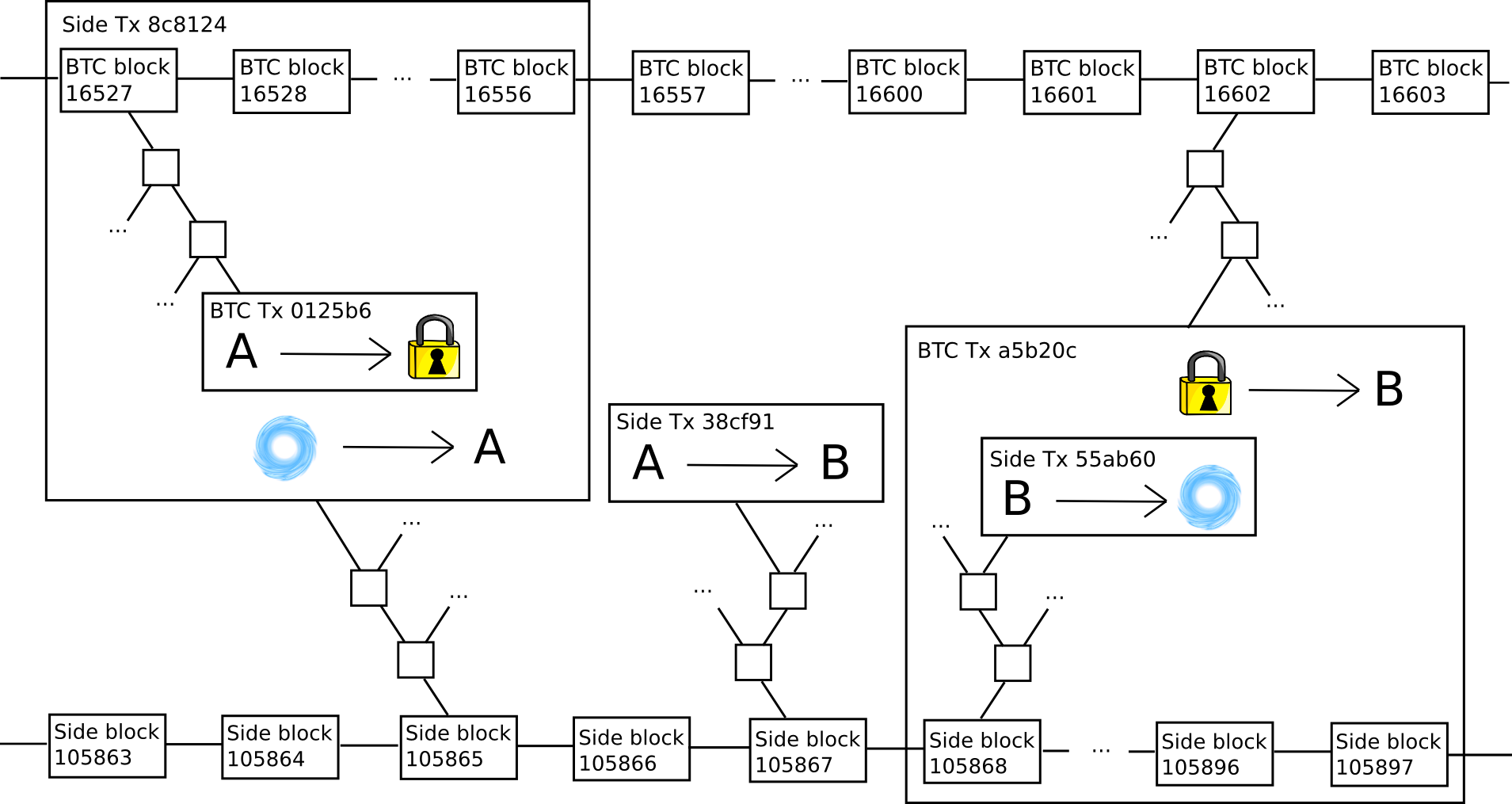

Sidechains are somewhat more complicated. The core underlying idea revolves around a “two-way-pegging” mechanism, where a “parent chain” (usually Bitcoin) and a “sidechain” share a common currency by making a unit of one convertible into a unit of the other. The way it works is as follows. First, in order to get a unit of side-coin, a user must send a unit of parent-coin into a special “lockbox script”, and then submit a cryptographic proof that this transaction took place into the sidechain. Once this transaction confirms, the user has the side-coin, and can send it at will. When any user holding a unit of side-coin wants to convert it back into parent-coin, they simply need to destroy the side-coin, and then submit a proof that this transaction took place to a lockbox script on the main chain. The lockbox script would then verify the proof, and if everything checks out it would unlock the parent-coin for the submitter of the side-coin-destroying transaction to spend.

Unfortunately, it is not practical to use the Bitcoin blockchain and currency at the same time; the basic technical reason is that nearly all interesting metacoins involve moving coins under more complex conditions than what the Bitcoin protocol itself supports, and so a separate “coin” is required (eg. MSC in Mastercoin, XCP in Counterparty). As we will see, each of these approaches has its own benefits, but it also has its own flaws. This point is important; particularly, note that many Bitcoin maximalists’ recent glee at Counterparty forking Ethereum was misplaced, as Counterparty-based Ethereum smart contracts cannot manipulate BTC currency units, and the asset that they are instead likely to promote (and indeed already have promoted) is the XCP.

Network Effects

Now, let us get to the primary argument at play here: network effects. In general, network effects can be defined simply: a network effect is a property of a system that makes the system intrinsically more valuable the more people use it. For example, a language has a strong network effect: Esperanto, even if it is technically superior to English in the abstract, is less useful in practice because the whole point of a language is to communicate with other people and not many other people speak Esperanto. On the other hand, a single road has a negative network effect: the more people use it the more congested it becomes.

In order to properly understand what network effects are at play in the cryptoeconomic context, we need to understand exactly what these network effects are, and exactly what thing each effect is attached to. Thus, to start off, let us list a few of the major ones (see here and here for primary sources):

Security effect: systems that are more widely adopted derive their consensus from larger consensus groups, making them more difficult to attack.

Payment system network effect: payment systems that are accepted by more merchants are more attractive to consumers, and payment systems used by more consumers are more attractive to merchants.

Developer network effect: there are more people interested in writing tools that work with platforms that are widely adopted, and the greater number of these tools will make the platform easier to use.

Integration network effect: third party platforms will be more willing to integrate with a platform that is widely adopted, and the greater number of these tools will make the platform easier to use.

Size stability effect: currencies with larger market cap tend to be more stable, and more established cryptocurrencies are seen as more likely (and therefore by self-fulfilling-prophecy actually are more likely) to remain at nonzero value far into the future.

Unit of account network effect: currencies that are very prominent, and stable, are used as a unit of account for pricing goods and services, and it is cognitively easier to keep track of one’s funds in the same unit that prices are measured in.

Market depth effect: larger currencies have higher market depth on exchanges, allowing users to convert larger quantities of funds in and out of that currency without taking a hit on the market price.

Market spread effect: larger currencies have higher liquidity (ie. lower spread) on exchanges, allowing users to convert back and forth more efficiently.

Intrapersonal single-currency preference effect: users that already use a currency for one purpose prefer to use it for other purposes both due to lower cognitive costs and because they can maintain a lower total liquid balance among all cryptocurrencies without paying interchange fees.

Interpersonal single-currency preference effect: users prefer to use the same currency that others are using to avoid interchange fees when making ordinary transactions

Marketing network effect: things that are used by more people are more prominent and thus more likely to be seen by new users. Additionally, users have more knowledge about more prominent systems and thus are less concerned that they might be exploited by unscrupulous parties selling them something harmful that they do not understand.

Regulatory legitimacy network effect: regulators are less likely to attack something if it is prominent because they will get more people angry by doing so

The first thing that we see is that these network effects are actually rather neatly split up into several categories: blockchain-specific network effects (1), platform-specific network effects (2-4), currency-specific network effects (5-10), and general network effects (11-12), which are to a large extent public goods across the entire cryptocurrency industry. There is a substantial opportunity for confusion here, since Bitcoin is simultaneously a blockchain, a currency and a platform, but it is important to make a sharp distinction between the three. The best way to delineate the difference is as follows:

A currency is something which is used as a medium of exchange or store of value; for example, dollars, BTC and DOGE.

A platform is a set of interoperating tools and infrastructure that can be used to perform certain tasks; for currencies, the basic kind of platform is the collection of a payment network and the tools needed to send and receive transactions in that network, but other kinds of platforms may also emerge.

A blockchain is a consensus-driven distributed database that modifies itself based on the content of valid transactions according to a set of specified rules; for example, the Bitcoin blockchain, the Litecoin blockchain, etc.

To see how currencies and platforms are completely separate, the best example to use is the world of fiat currencies. Credit cards, for example, are a highly multi-currency platform. Someone with a credit card from Canada tied to a bank account using Canadian dollars can spend funds at a merchant in Switzerland accepting Swiss francs, and both sides barely know the difference. Meanwhile, even though both are (or at least can be) based on the US dollar, cash and Paypal are completely different platforms; a merchant accepting only cash will have a hard time with a customer who only has a Paypal account.

As for how platforms and blockchains are separate, the best example is the Bitcoin payment protocol and proof of existence. Although the two use the same blockchain, they are completely different applications, users of one have no idea how to interpret transactions associated with the other, and it is relatively easy to see how they benefit from completely different network effects so that one can easily catch on without the other. Note that protocols like proof of existence and Factom are mostly exempt from this discussion; their purpose is to embed hashes into the most secure available ledger, and while a better ledger has not materialized they should certainly use Bitcoin, particularly because they can use Merkle trees to compress a large number of proofs into a single hash in a single transaction.

Network Effects and Metacoins

Now, in this model, let us examine metacoins and sidechains separately. With metacoins, the situation is simple: metacoins are built on Bitcoin the blockchain, and not Bitcoin the platform or Bitcoin the currency. To see the former, note that users need to download a whole new set of software packages in order to be able to process Bitcoin transactions. There is a slight cognitive network effect from being able to use the same old infrastructure of Bitcoin private/public key pairs and addresses, but this is a network effect for the combination of ECDSA, SHA256+RIPEMD160 and base 58 and more generally the whole concept of cryptocurrency, not the Bitcoin platform; Dogecoin inherits exactly the same gains. To see the latter, note that, as mentioned above, Counterparty has its own internal currency, the XCP. Hence, metacoins benefit from the network effect of Bitcoin’s blockchain security, but do not automatically inherit all of the platform-specific and currency-specific network effects.

Of course, metacoins’ departure from the Bitcoin platform and Bitcoin currency is not absolute. First of all, even though Counterparty is not “on” the Bitcoin platform, it can in a very meaningful sense be said to be “close” to the Bitcoin platform – one can exchange back and forth between BTC and XCP very cheaply and efficiently. Cross-chain centralized or decentralized exchange, while possible, is several times slower and more costly. Second, some features of Counterparty, particularly the token sale functionality, do not rely on moving currency units under any conditions that the Bitcoin protocol does not support, and so one can use that functionality without ever purchasing XCP, using BTC directly. Finally, transaction fees in all metacoins can be paid in BTC, so in the case of purely non-financial applications metacoins actually do fully benefit from Bitcoin’s currency effect, although we should note that in most non-financial cases developers are used to messaging being free, so convincing anyone to use a non-financial blockchain dapp at $ 0.05 per transaction will likely be an uphill battle.

In some of these applications – particularly, perhaps to Bitcoin maximalists’ chagrin, Counterparty’s crypto 2.0 token sales, the desire to move back and forth quickly to and from Bitcoin, as well as the ability to use it directly, may indeed create a platform network effect that overcomes the loss of secure light client capability and potential for blockchain speed and scalability upgrades, and it is in these cases that metacoins may find their market niche. However, metacoins are most certainly not an all-purpose solution; it is absurd to believe that Bitcoin full nodes will have the computational ability to process every single crypto transaction that anyone will ever want to do, and so eventually movement to either scalable architectures or multichain environments will be necessary.

Network Effects and Sidechains

Sidechains have the opposite properties of metacoins. They are built on Bitcoin the currency, and thus benefit from Bitcoin’s currency network effects, but they are otherwise exactly identical to fully independent chains and have the same properties. This has several pros and cons. On the positive side, it means that, although “sidechains” by themselves are not a scalability solution as they do not solve the security problem, future advancements in multichain, sharding or other scalability strategies are all open to them to adopt.

On the negative side, however, they do not benefit from Bitcoin’s platform network effects. One must download special software in order to be able to interact with a sidechain, and one must explicitly move one’s bitcoins onto a sidechain in order to be able to use it – a process wich is equally as difficult as converting them into a new currency in a new network via a decentralized exchange. In fact, Blockstream employees have themselves admitted that the process for converting side-coins back into bitcoins is relatively inefficient, to the point that most people seeking to move their bitcoins there and back will in fact use exactly the same centralized or decentralized exchange processes as would be used to migrate to a different currency on an independent blockchain.

Additionally, note that there is one security approach that independent networks can use which is not open to sidechains: proof of stake. The reasons for this are twofold. First one of the key arguments in favor of proof of stake is that even a successful attack against proof of stake will be costly for the attacker, as the attacker will need to keep his currency units deposited and watch their value drop drastically as the market realizes that the coin is compromised. This incentive effect does not exist if the only currency inside of a network is pegged to an external asset whose value is not so closely tied to that network’s success.

Second, proof of stake gains much of its security because the process of buying up 50% of a coin in order to mount a takeover attack will itself increase the coin’s price drastically, making the attack even more expensive for the attacker. In a proof of stake sidechain, however, one can easily move a very large quantity of coins into a chain from the parent chain, an mount the attack without moving the asset price at all. Note that both of these arguments continue to apply even if Bitcoin itself upgrades to proof of stake for its security. Hence, if you believe that proof of stake is the future, then both metacoins and sidechains (or at least pure sidechains) become highly suspect, and thus for that purely technical reason Bitcoin maximalism (or, for that matter, ether maximalism, or any other kind of currency maximalism) becomes dead in the water.

Currency Network Effects, Revisited

Altogether, the conclusion from the above two points is twofold. First, there is no universal and scalable approach that allows users to benefit from Bitcoin’s platform network effects. Any software solution that makes it easy for Bitcoin users to move their funds to sidechains can be easily converted into a solution that makes it just as easy for Bitcoin users to convert their funds into an independent currency on an independent chain. On the other hand, however, currency network effects are another story, and may indeed prove to be a genuine advantage for Bitcoin-based sidechains over fully independent networks. So, what exactly are these effects and how powerful is each one in this context? Let us go through them again:

Size-stability network effect (larger currencies are more stable) – this network effect is legitimate, and Bitcoin has been shown to be less volatile than smaller coins.

Unit of account network effect (very large currencies become units of account, leading to more purchasing power stability via price stickiness as well as higher salience) – unfortunately, Bitcoin will likely never be stable enough to trigger this effect; the best empirical evidence we can see for this is likely the valuation history of gold.

Market depth effect (larger currencies support larger transactions without slippage and have a lower bid/ask spread) – these effect are legitimate up to a point, but then beyond that point (perhaps a market cap of $ 10-$ 100M), the market depth is imply good enough and the spread is low enough for nearly all types of transactions, and the benefit from further gains is small.

Single-currency preference effect (people prefer to deal with fewer currencies, and prefer to use the same currencies that others are using) – the intrapersonal and interpersonal parts to this effect are legitimate, but we note that (i) the intrapersonal effect only applies within individual people, not between people, so it does not prevent an ecosystem with multiple preferred global currencies from existing, and (ii) the interpersonal effect is small as interchange fees especially in crypto tend to be very low, less than 0.30%, and will likely go down to essentially zero with decentralized exchange.

Hence, the single-currency preference effect is likely the largest concern, followed by the size stability effects, whereas the market depth effects are likely relatively tiny once a cryptocurrency gets to a substantial size. However, it is important to note that the above points have several major caveats. First, if (1) and (2) dominate, then we know of explicit strategies for making a new coin that is even more stable than Bitcoin even at a smaller size; thus, they are certainly not points in Bitcoin’s favor.

Second, those same strategies (particularly the exogenous ones) can actually be used to create a stable coin that is pegged to a currency that has vastly larger network effects than even Bitcoin itself; namely, the US dollar. The US dollar is thousands of times larger than Bitcoin, people are already used to thinking in terms of it, and most importantly of all it actually maintains its purchasing power at a reasonable rate in the short to medium term without massive volatility. Employees of Blockstream, the company behind sidechains, have often promoted sidechains under the slogan “innovation without speculation“; however, the slogan ignores that Bitcoin itself is quite speculative and as we see from the experience of gold always will be, so seeking to install Bitcoin as the only cryptoasset essentially forces all users of cryptoeconomic protocols to participate in speculation. Want true innovation without speculation? Then perhaps we should all engage in a little US dollar stablecoin maximalism instead.

Finally, in the case of transaction fees specifically, the intrapersonal single-currency preference effect arguably disappears completely. The reason is that the quantities involved are so small ($ 0.01-$ 0.05 per transaction) that a dapp can simply siphon off $ 1 from a user’s Bitcoin wallet at a time as needed, not even telling the user that other currencies exist, thereby lowering the cognitive cost of managing even thousands of currencies to zero. The fact that this token exchange is completely non-urgent also means that the client can even serve as a market maket while moving coins from one chain to the other, perhaps even earning a profit on the currency interchange bid/ask spread. Furthermore, because the user does not see gains and losses, and the user’s average balance is so low that the central limit theorem guarantees with overwhelming probability that the spikes and drops will mostly cancel each other out, stability is also fairly irrelevant. Hence, we can make the point that alternative tokens which are meant to serve primarily as “cryptofuels” do not suffer from currency-specific network effect deficiencies at all. Let a thousand cryptofuels bloom.

Incentive and Psychological Arguments

There is another class of argument, one which may perhaps be called a network effect but not completely, for why a service that uses Bitcoin as a currency will perform better: the incentivized marketing of the Bitcoin community. The argument goes as follows. Services and platforms based on Bitcoin the currency (and to a slight extent services based on Bitcoin the platform) increase the value of Bitcoin. Hence, Bitcoin holders would personally benefit from the value of their BTC going up if the service gets adopted, and are thus motivated to support it.

This effect occurs on two levels: the individual and the corporate. The corporate effect is a simple matter of incentives; large businesses will actually support or even create Bitcoin-based dapps to increase Bitcoin’s value, simply because they are so large that even the portion of the benefit that personally accrues to themselves is enough to offset the costs; this is the “speculative philanthropy” strategy described by Daniel Krawisz.

The individual effect is not so much directly incentive-based; each individual’s ability to affect Bitcoin’s value is tiny. Rather, it’s more a clever exploitation of psychological biases. It’s well-known that people tend to change their moral values to align with their personal interests, so the channel here is more complex: people who hold BTC start to see it as being in the common interest for Bitcoin to succeed, and so they will genuinely and excitedly support such applications. As it turns out, even a small amount of incentive suffices to shift over people’s moral values to such a large extent, creating a psychological mechanism that manages to overcome not just the coordination problem but also, to a weak extent, the public goods problem.

There are several major counterarguments to this claim. First, it is not at all clear that the total effect of the incentive and psychological mechanisms actually increases as the currency gets larger. Although a larger size leads to more people affected by the incentive, a smaller size creates a more concentrated incentive, as people actually have the opportunity to make a substantial difference to the success of the project. The tribal psychology behind incentive-driven moral adjustment may well be stronger for small “tribes” where individuals also have strong social connections to each other than larger tribes where such connections are more diffuse; this is somewhat similar to the Gemeinschaft vs Gesellschaft distinction in sociology. Perhaps a new protocol needs to have a concentrated set of highly incentivized stakeholders in order to seed a community, and Bitcoin maximalists are wrong to try to knock this ladder down after Bitcoin has so beautifully and successfully climbed up it. In any case, all of the research around optimum currency areas will have to be heavily redone in the context of the newer volatile cryptocurrencies, and the results may well go down either way.

Second, the ability for a network to issue units of a new coin has been proven to be a highly effective and successful mechanism for solving the public goods problem of funding protocol development, and any platform that does not somehow take advantage of the seignorage revenue from creating a new coin is at a substantial disadvantage. So far, the only major crypto 2.0 protocol-building company that has successfully funded itself without some kind of “pre-mine” or “pre-sale” is Blockstream (the company behind sidechains), which recently received $ 21 million of venture capital funding from Silicon Valley investors. Given Blockstream’s self-inflicted inability to monetize via tokens, we are left with three viable explanations for how investors justified the funding:

The funding was essentially an act of speculative philathropy on the part of Silicon Valley venture capitalists looking to increase the value of their BTC and their other BTC-related investments.

Blockstream intends to earn revenue by taking a cut of the fees from their blockchains (non-viable because the public will almost certainly reject such a clear and blatant centralized siphoning of resources even more virulently then they would reject a new currency)

Blockstream intends to “sell services”, ie. follow the RedHat model (viable for them but few others; note that the total room in the market for RedHat-style companies is quite small)

Both (1) and (3) are highly problematic; (3) because it means that few other companies will be able to follow its trail and because it gives them the incentive to cripple their protocols so they can provide centralized overlays, and (1) because it means that crypto 2.0 companies must all follow the model of sucking up to the particular concentrated wealthy elite in Silicon Valley (or maybe an alternative concentrated wealthy elite in China), hardly a healthy dynamic for a decentralized ecosystem that prides itself on its high degree of political independence and its disruptive nature.

Ironically enough, the only “independent” sidechain project that has so far announced itself, Truthcoin, has actually managed to get the best of both worlds: the project got on the good side of the Bitcoin maximalist bandwagon by announcing that it will be are a sidechain, but in fact the development team intends to introduce into the platform two “coins” – one of which will be a BTC sidechain token and the other an independent currency that is meant to be, that’s right, crowd-sold.

A New Strategy

Thus, we see that while currency network effects are sometimes moderately strong, and they will indeed exert a preference pressure in favor of Bitcoin over other existing cryptocurrencies, the creation of an ecosystem that uses Bitcoin exclusively is a highly suspect endeavor, and one that will lead to a total reduction and increased centralization of funding (as only the ultra-rich have sufficient concentrated incentive to be speculative philanthropists), closed doors in security (no more proof of stake), and is not even necessarily guaranteed to end with Bitcoin willing. So is there an alternative strategy that we can take? Are there ways to get the best of both worlds, simultaneously currency network effects and securing the benefits of new protocols launching their own coins?

As it turns out, there is: the dual-currency model. The dual-currency model, arguably pioneered by Robert Sams, although in various incarnations independently discovered by Bitshares, Truthcoin and myself, is at the core simple: every network will contain two (or even more) currencies, splitting up the role of medium of transaction and vehicle of speculation and stake (the latter two roles are best merged, because as mentioned above proof of stake works best when participants suffer the most from a fork). The transactional currency will be either a Bitcoin sidechain, as in Truthcoin’s model, or an endogenous stablecoin, or an exogenous stablecoin that benefits from the almighty currency network effect of the US dollar (or Euro or CNY or SDR or whatever else). Hayekian currency competition will determine which kind of Bitcoin, altcoin or stablecoin users prefer; perhaps sidechain technology can even be used to make one particular stablecoin transferable across many networks.

The vol-coin will be the unit of measurement of consensus, and vol-coins will sometimes be absorbed to issue new stablecoins when stablecoins are consumed to pay transaction fees; hence, as explainted in the argument in the linked article on stablecoins, vol-coins can be valued as a percentage of future transaction fees. Vol-coins can be crowd-sold, maintaining the benefits of a crowd sale as a funding mechanism. If we decide that explicit pre-mines or pre-sales are “unfair”, or that they have bad incentives because the developers’ gain is frontloaded, then we can instead use voting (as in DPOS) or prediction markets instead to distribute coins to developers in a decentralized way over time.

Another point to keep in mind is, what happens to the vol-coins themselves? Technological innovation is rapid, and if each network gets unseated within a few years, then the vol-coins may well never see substantial market cap. One answer is to solve the problem by using a clever combination of Satoshian thinking and good old-fashioned recursive punishment systems from the offline world: establish a social norm that every new coin should pre-allocate 50-75% of its units to some reasonable subset of the coins that came before it that directly inspired its creation, and enforce the norm blockchain-style – if your coin does not honor its ancestors, then its descendants will refuse to honor it, instead sharing the extra revenues between the originally cheated ancestors and themselves, and no one will fault them for that. This would allow vol-coins to maintain continuity over the generations. Bitcoin itself can be included among the list of ancestors for any new coin. Perhaps an industry-wide agreement of this sort is what is needed to promote the kind of cooperative and friendly evolutionary competition that is required for a multichain cryptoeconomy to be truly successful.

Would we have used a vol-coin/stable-coin model for Ethereum had such strategies been well-known six months ago? Quite possibly yes; unfortunately it’s too late to make the decision now at the protocol level, particularly since the ether genesis block distribution and supply model is essentially finalized. Fortunately, however, Ethereum allows users to create their own currencies inside of contracts, so it is entirely possible that such a system can simply be grafted on, albeit slightly unnaturally, over time. Even without such a change, ether itself will retain a strong and steady value as a cryptofuel, and as a store of value for Ethereum-based security deposits, simply because of the combination of the Ethereum blockchain’s network effect (which actually is a platform network effect, as all contracts on the Ethereum blockchain have a common interface and can trivially talk to each other) and the weak-currency-network-effect argument described for cryptofuels above preserves for it a stable position. For 2.0 multichain interaction, however, and for future platforms like Truthcoin, the decision of which new coin model to take is all too relevant.

Kaum ein Altcoin wurde mit so viel Gedöns und Begeisterung verkündet wie Ethereum. Aber was ist dran an dem System, das, so die Medien, “alles” dezentralisieren. ethereum – Google Blogsuche

Wir können Cookies anfordern, die auf Ihrem Gerät eingestellt werden. Wir verwenden Cookies, um uns mitzuteilen, wenn Sie unsere Websites besuchen, wie Sie mit uns interagieren, Ihre Nutzererfahrung verbessern und Ihre Beziehung zu unserer Website anpassen.

Klicken Sie auf die verschiedenen Kategorienüberschriften, um mehr zu erfahren. Sie können auch einige Ihrer Einstellungen ändern. Beachten Sie, dass das Blockieren einiger Arten von Cookies Auswirkungen auf Ihre Erfahrung auf unseren Websites und auf die Dienste haben kann, die wir anbieten können.

Notwendige Website Cookies

Diese Cookies sind unbedingt erforderlich, um Ihnen die auf unserer Webseite verfügbaren Dienste und Funktionen zur Verfügung zu stellen.

Da diese Cookies für die auf unserer Webseite verfügbaren Dienste und Funktionen unbedingt erforderlich sind, hat die Ablehnung Auswirkungen auf die Funktionsweise unserer Webseite. Sie können Cookies jederzeit blockieren oder löschen, indem Sie Ihre Browsereinstellungen ändern und das Blockieren aller Cookies auf dieser Webseite erzwingen. Sie werden jedoch immer aufgefordert, Cookies zu akzeptieren / abzulehnen, wenn Sie unsere Website erneut besuchen.

Wir respektieren es voll und ganz, wenn Sie Cookies ablehnen möchten. Um zu vermeiden, dass Sie immer wieder nach Cookies gefragt werden, erlauben Sie uns bitte, einen Cookie für Ihre Einstellungen zu speichern. Sie können sich jederzeit abmelden oder andere Cookies zulassen, um unsere Dienste vollumfänglich nutzen zu können. Wenn Sie Cookies ablehnen, werden alle gesetzten Cookies auf unserer Domain entfernt.

Wir stellen Ihnen eine Liste der von Ihrem Computer auf unserer Domain gespeicherten Cookies zur Verfügung. Aus Sicherheitsgründen können wie Ihnen keine Cookies anzeigen, die von anderen Domains gespeichert werden. Diese können Sie in den Sicherheitseinstellungen Ihres Browsers einsehen.

Andere externe Dienste

Wir nutzen auch verschiedene externe Dienste wie Google Webfonts, Google Maps und externe Videoanbieter. Da diese Anbieter möglicherweise personenbezogene Daten von Ihnen speichern, können Sie diese hier deaktivieren. Bitte beachten Sie, dass eine Deaktivierung dieser Cookies die Funktionalität und das Aussehen unserer Webseite erheblich beeinträchtigen kann. Die Änderungen werden nach einem Neuladen der Seite wirksam.

Google Webfont Einstellungen:

Google Maps Einstellungen:

Google reCaptcha Einstellungen:

Vimeo und YouTube Einstellungen:

Datenschutzrichtlinie

Sie können unsere Cookies und Datenschutzeinstellungen im Detail in unseren Datenschutzrichtlinie nachlesen.

{kind=link}

{kind=link}